Benefits of Owning a Freehold Property in Singapore

One of the key benefits for owning a freehold property is the perpetuity of ownership that grants the owner the peace of mind that the lease will never run out. Such properties are especially useful for legacy planning because they allow owners to pass them down from generation to generation since there is no time limit to their ownership. A word of caution – It is still possible for governing bodies to take back that land for national development projects. So, make sure to take a long-term view when selecting the properties to avoid land locations that are more likely to cross paths with national infrastructures such as train lines or communication networks.

Another benefit for perpetual ownership lies in the ease of on-going financing. In Singapore, banks require properties to have at least 30 years of remaining tenure. The amount of financing that these banks can provide, also known as Loan to Value (LTV) ratio, can be significantly lowered if the property starts to age. As such, buyers for properties with limited tenure can access fewer financing options, consequently restricting the owners’ ability to sell their properties. However, owners of freehold properties are free from such a problem because of their infinite ownership.

Additionally, the sale price of a new freehold condo unit can be 10 to 15% higher when compared to a leasehold unit in the same area. Because of the prestige and perceived value that are tagged to freehold properties, they are usually one of the more sought-after property types in Singapore.

Does Freehold Mean I Own the Land?

The answer is yes and no, it all depends on the property type.

If it is a landed property such as Detached house, Semi-detached house, Terrace House or Good Class Bungalows (GCBs), the owner of the property is essentially the owner of the land too.

For freehold condominiums and cluster houses however, the individual unit owners are not the landowner.

The lands in which multiple property units are built are held by the Management Corporation Strata Title (MCST). Such an entity is empowered by the law to administer and oversee the common property of strata developments such as private condominiums, shopping centres and industrial facilities to fulfil management duties under the Building Maintenance and Strata Management Act (Chapter 30C). In short, it serves as a managing agent to upkeeping the property and facilities in compliance with the Act.

What Does En-bloc Mean?

A collective sale, also known as an en-bloc, refers to a sale of two or more property units to a common developer. This occurs when a developer wants to buy up the land on which an existing property stands and redevelop it as a new estate.

What Are the Factors Affecting En-bloc Potential?

1. Condo Plot Ratio

The key factor that can affect en-bloc potential is plot ratio. It determines the height of developments and the number of residential units that can be built. Primarily, developers favour old condos with under-utilised plot ratios so that they can build more residential units than the existing development to reap a greater profit margin.

2. Development Location

The location and the land size also play a huge part in gaining developers’ interest because they can affect the marketability and profitability of the new development. A prime location can naturally draw buyers with its convenience, however, if the land size is too big, developers might be threatened by the additional government tax and charges that they will incur if the development is not built and sold out within five years of obtaining the land.

3. Tenure

Tenure is another indicator for en-bloc potential because the older the property, the more likely to be the target of collective sales and easier for the developer to round up enough residentials to agree to the sale. As a rule of thumb, for a development that is older than 10 years, only 80% of its owners need to agree to sell their homes before the collective sale can take place. For developments less than 10 years, the percentage increases to 90%.

4. Well-Developed Neighborhood

A well-developed neighbourhood such as one with improved accessibility such as new train stations, amenities and rising prices in other property developments in the vicinity can also signal a potential for en-bloc because development in such areas are more marketable and developers can price their projects higher for greater profit.

Enbloc Cycle in Singapore

The en-bloc cycle seems to run on a 10-year cycle. The first wave occurred in 1997 with almost 100 collective sales completed in the three years preceding, and the second happened in 2007 when almost 170 en-bloc deals worth $12.61 billion were closed in one single year. The most recent wave that occurred in 2017 also witnessed at least 37 tenders.

In general, developers tend to favour freehold properties for their en-bloc initiatives because the Government Land Sales (GLS) is no longer releasing freehold plots to developers, hence buying over old freehold properties through collective sales are the only possibilities for regaining these lands. Nevertheless, these are win-win situations for developers to acquire freehold plots and property owners to profit from these collective sales that tend to offer higher prices.

Is En-bloc Potential a Factor to Consider When Purchasing a Property?

Again, the answer is yes and no because it all depends on the buyers’ objective and preference. Besides, with the 2018 cooling measure that imposes 30% Additional Buyer’s Stamp Duty (ABSD) on developers purchasing residential properties, en-bloc may be harder to come by.

With the ever-changing Singapore property market, buyers should conduct substantial research and analysis before embarking on their buying spree. When in doubt, reach out to our experts to tap on their insights

Should I Buy a Freehold Condo with En-bloc Potential?

While the potential to reap a profit from an en-bloc sale is attractive, this should not be the key deciding factor for purchasing a freehold condo. Before making the purchase, why not consider the objectives for the purchase of a property and different lifestyle of the occupants? Such exercise can often reveal suitable alternatives that are not considered before.

List of Freehold Condo we think with a En-bloc Potential

If freehold condos with en-bloc potential are still on top of the buying list, here are some possible options we think have a good En-bloc potential:

| PROPERTY | TENURE | DISTRICT | NO. OF UNITS | TOP YEAR | |||

|---|---|---|---|---|---|---|---|

| GLORIA MANSION | FREEHOLD | D5 / QUEENSTOWN | 31 UNITS | 1995 | |||

| CAIRNHILL ASTORIA | FREEHOLD | D9 / NEWTON | 36 UNITS | 1983 | |||

| SPANISH VILLAGE | FREEHOLD | D10 / TANGLIN | 226 UNITS | 1987 | |||

| BALMORAL POINT | FREEHOLD | D10 / TANGLIN | 31 UNITS | 1974 | |||

| GRANGE HEIGHTS | FREEHOLD | D9 / RIVER VALLEY | 120 UNITS | 1975 | |||

| EAST GROVE | FREEHOLD | D15 / BEDOK | 36 UNITS | 1975 | |||

| HIGH POINT | FREEHOLD | D9 / NEWTON | 59 UNITS | 1974 | |||

| STILL MANSIONS | FREEHOLD | D15 / BEDOK | 30 UNITS | 1967 |

Buying a property based on the en-bloc potential alone can be a real gamble for buyers because there is no guarantee of such collective sales or when it will happen. In Singapore, there are many property options to suit different needs, contact our trusted agents now and let them assist you in your search for that ideal property.

Disclaimer: The list of condos and content article does not take into account of your personal investment and property purchase objectives and does not constitute property purchase or investment advise. The information are not intended to be and do not constitute property advice, investment advice, property investment advice or any other advice or recommendation of any sort offered or endorsed by Prop.sg also does not warrant that such information and publications are accurate, up to date or applicable to the circumstances of any particular case.

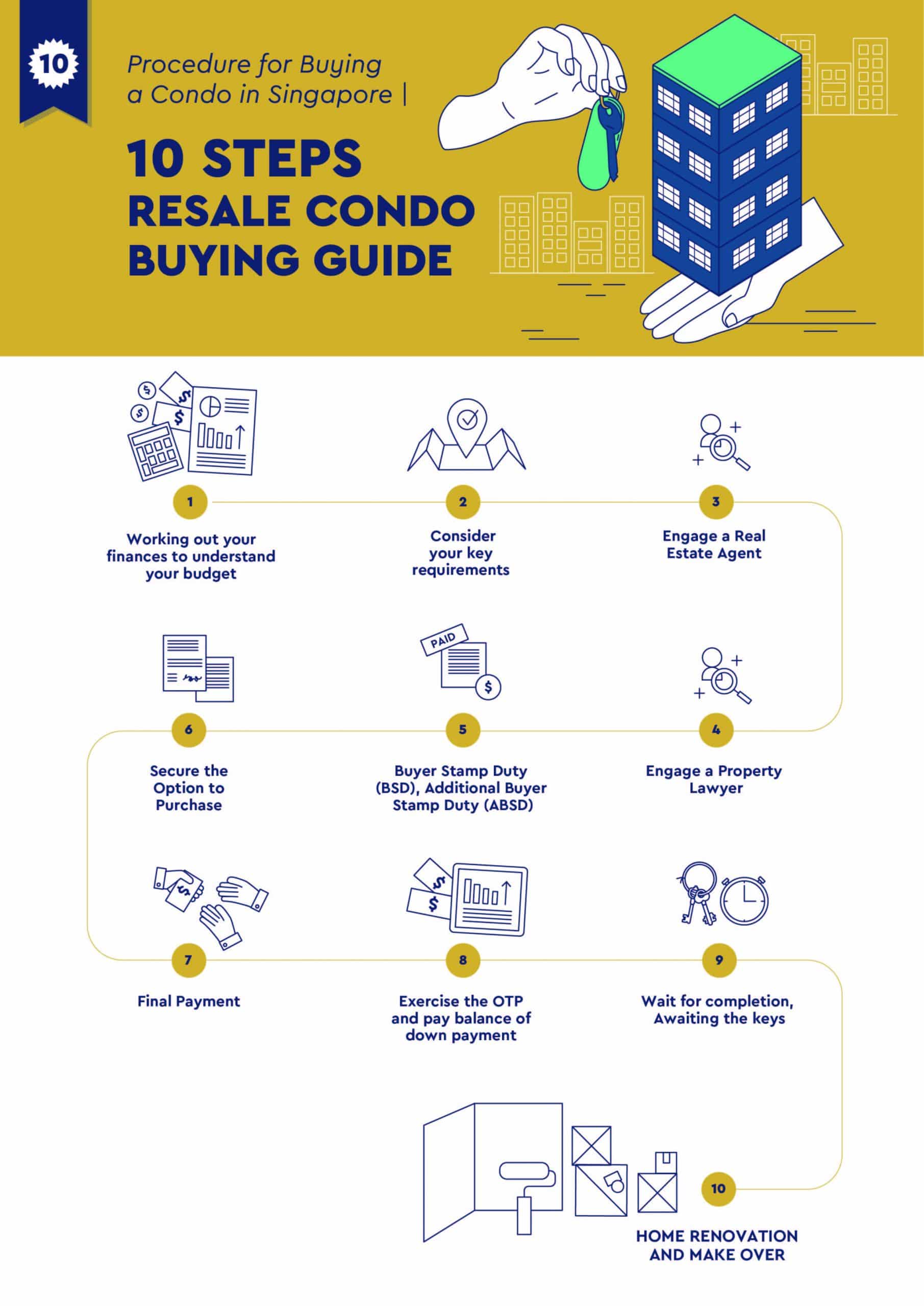

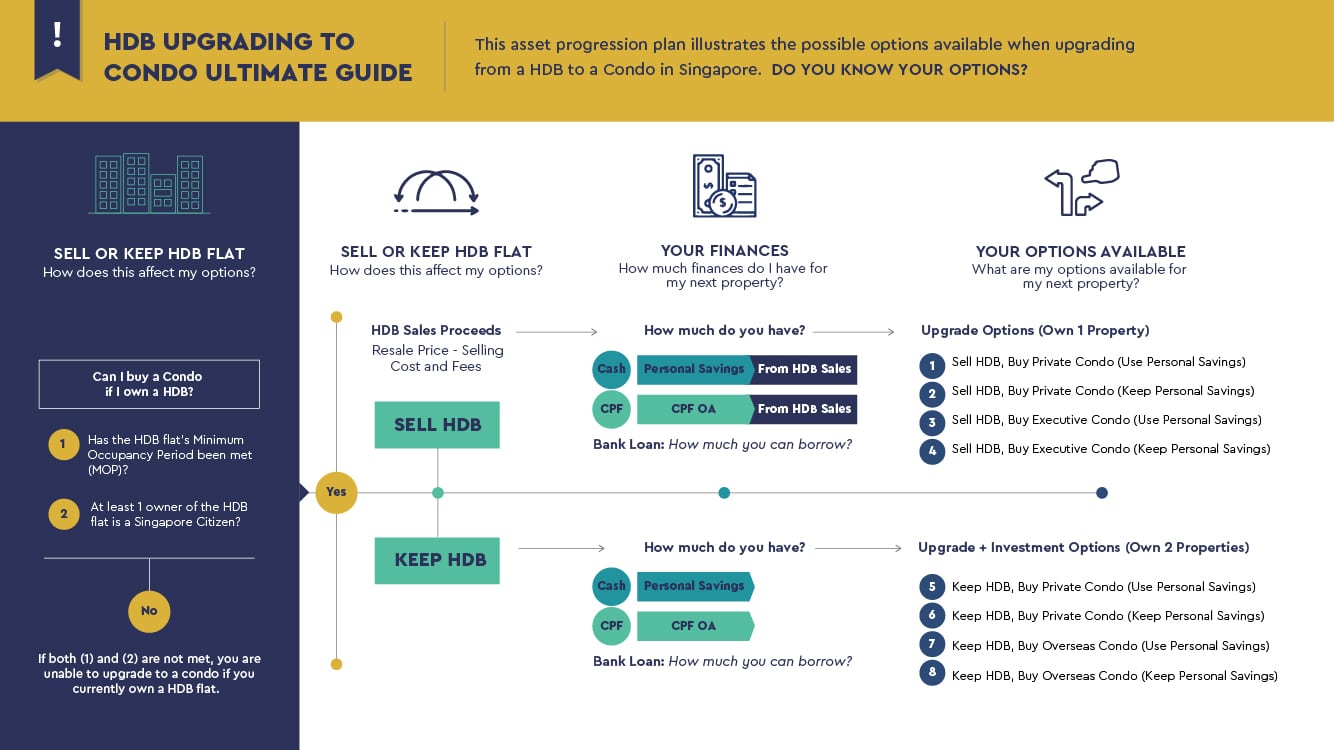

Before you begin, you ought to consider your eligibility in purchasing or upgrading to a condominium. You will only be able to buy a condominium if you have met the following requirements: reaching the Minimum Occupancy Period (MOP) of living in your HDB for five years and above, and that at least one of the registered homeowners is a Singaporean Citizen.

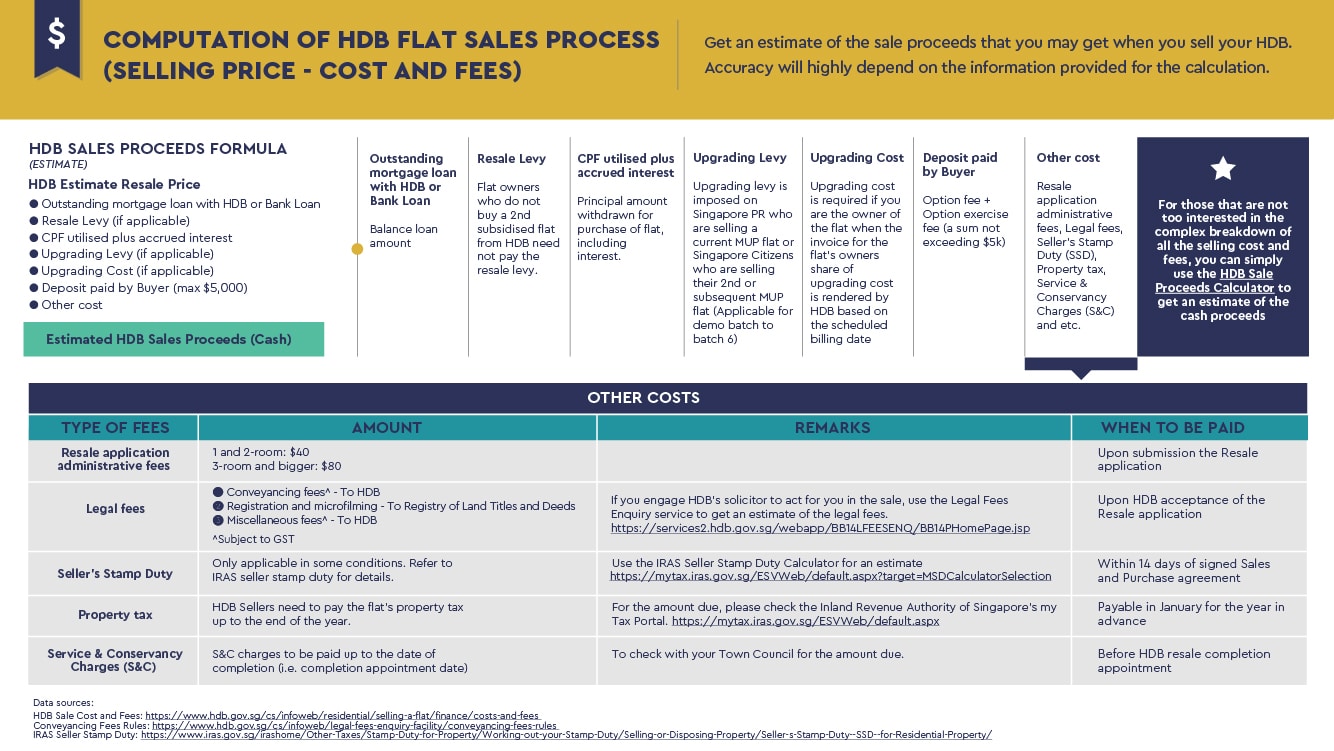

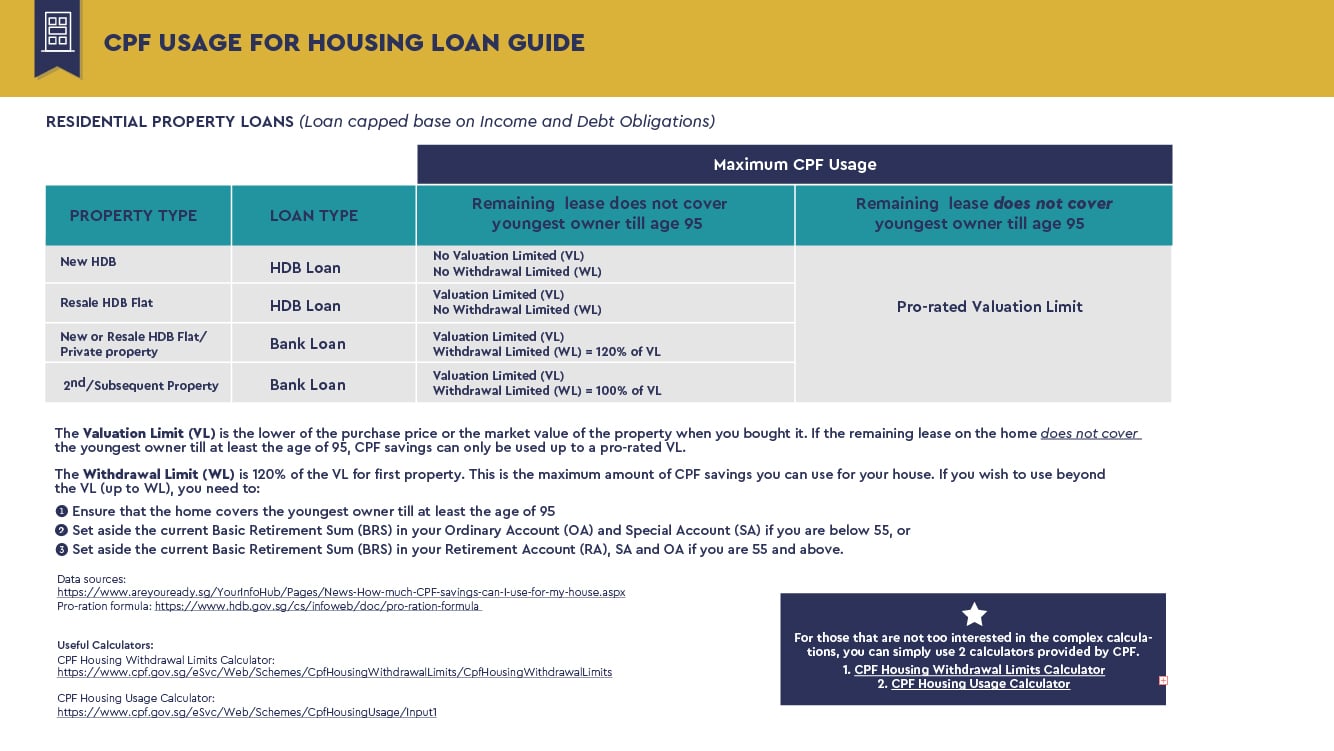

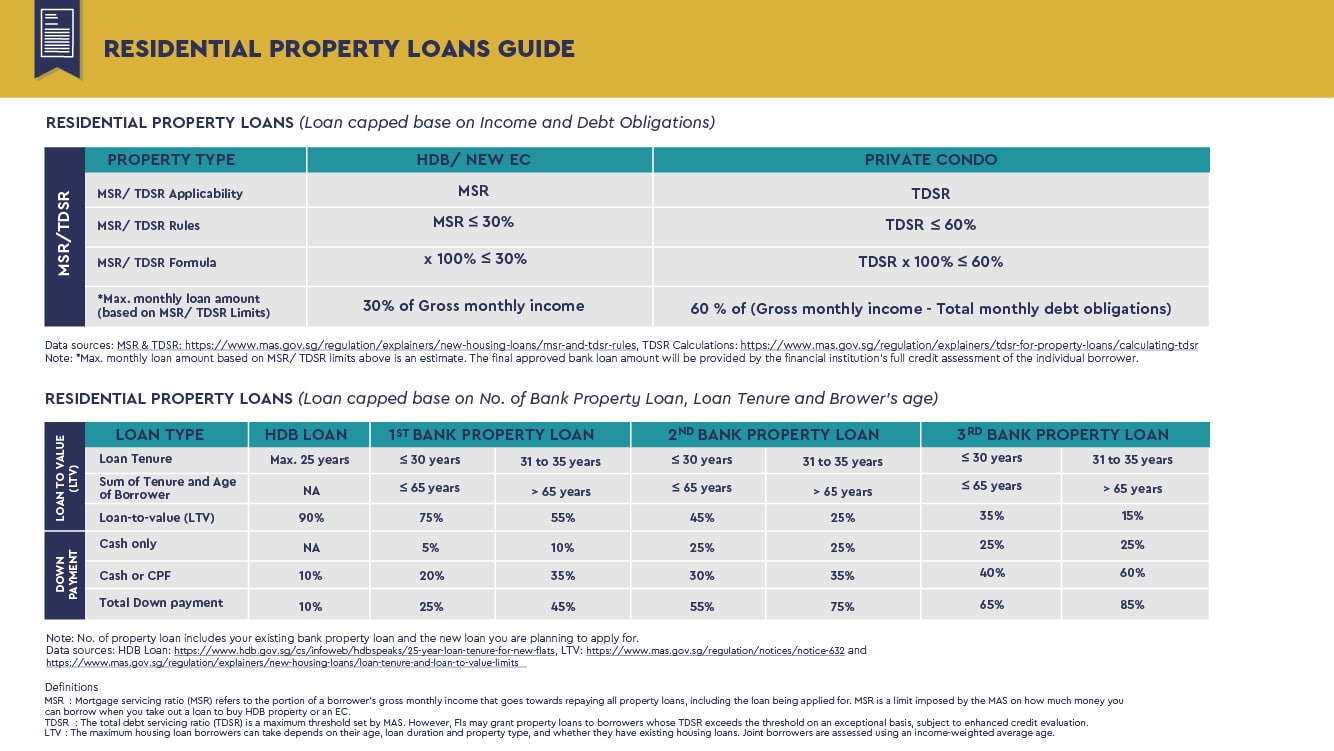

Once you have cleared these requirements, you may begin to contemplate if you wish to retain or sell your flat. There are these four basic sources for you to fund your purchase: cash, personal savings, Central Provident Fund (CPF) from the Ordinary Account as well as taking a bank loan. You have to consider how readily available these funds are to you before you proceed to purchase your new home. For instance, bank loans are dependent on your income, determining how much the bank is willing to provide you with a loan. Selling your flat will allow you to properly fund your purchase of a condominium, with sales proceeds as another channel to being able to pay for it.

Should you choose to sell your HDB and upgrade, you may purchase either a private condominium or an executive condominium with the option of using or keeping your personal savings. On the other hand, keeping your HDB allows you to purchase either a private condominium or an overseas condominium, also with the option of using or keeping your personal savings. In totality, selling your HDB renders you with one property, while keeping it leaves you with two properties under your name. And there you have it, a basic overview of purchasing a condominium. If you have any further queries, feel free to contact us, with a no obligation, no charge consultation on the options available to you.

Before you begin, you ought to consider your eligibility in purchasing or upgrading to a condominium. You will only be able to buy a condominium if you have met the following requirements: reaching the Minimum Occupancy Period (MOP) of living in your HDB for five years and above, and that at least one of the registered homeowners is a Singaporean Citizen.

Once you have cleared these requirements, you may begin to contemplate if you wish to retain or sell your flat. There are these four basic sources for you to fund your purchase: cash, personal savings, Central Provident Fund (CPF) from the Ordinary Account as well as taking a bank loan. You have to consider how readily available these funds are to you before you proceed to purchase your new home. For instance, bank loans are dependent on your income, determining how much the bank is willing to provide you with a loan. Selling your flat will allow you to properly fund your purchase of a condominium, with sales proceeds as another channel to being able to pay for it.

Should you choose to sell your HDB and upgrade, you may purchase either a private condominium or an executive condominium with the option of using or keeping your personal savings. On the other hand, keeping your HDB allows you to purchase either a private condominium or an overseas condominium, also with the option of using or keeping your personal savings. In totality, selling your HDB renders you with one property, while keeping it leaves you with two properties under your name. And there you have it, a basic overview of purchasing a condominium. If you have any further queries, feel free to contact us, with a no obligation, no charge consultation on the options available to you.