How to Upgrade from HDB to Condo in Singapore: The Complete 2026 Guide

Upgrading from HDB to condo in 2026? Learn the sell-first vs buy-first ABSD strategy, the 20% ABSD, LTV, TDSR, MSR and property-tax rules before you commit.

Key takeaways

- You can keep your HDB flat and buy a condo only after the 5-year Minimum Occupation Period (MOP) and if at least one owner is a Singapore Citizen, otherwise the flat must be sold within 6 months.

- The two clean upgrader routes are: sell your HDB first then buy the condo (no ABSD), or buy the condo first, pay ABSD upfront, then sell your HDB within 6 months to claim the married-couple ABSD remission.

- ABSD on a Singapore Citizen's second residential property is 20% (since 27 April 2023), so paying it first and clawing it back later ties up serious cash.

- Borrowing is capped by a 75% bank LTV on your first loan, TDSR of 55% (stress-tested at a 4% interest floor), and a 30% MSR if you go for an HDB flat or a developer EC.

- If you keep the old flat and rent it out, expect higher non-owner-occupier property tax (12% to 36%) on it, not the owner-occupier rates.

Public housing is the most common form of housing ownership here in Singapore, with over 80% of Singaporeans residing in one. Yet, there are also private homes, and upgrading to one is often seen as a milestone. After living in your HDB flat for a while, it may have crossed your mind to either upgrade or purchase a private home, namely a condominium.

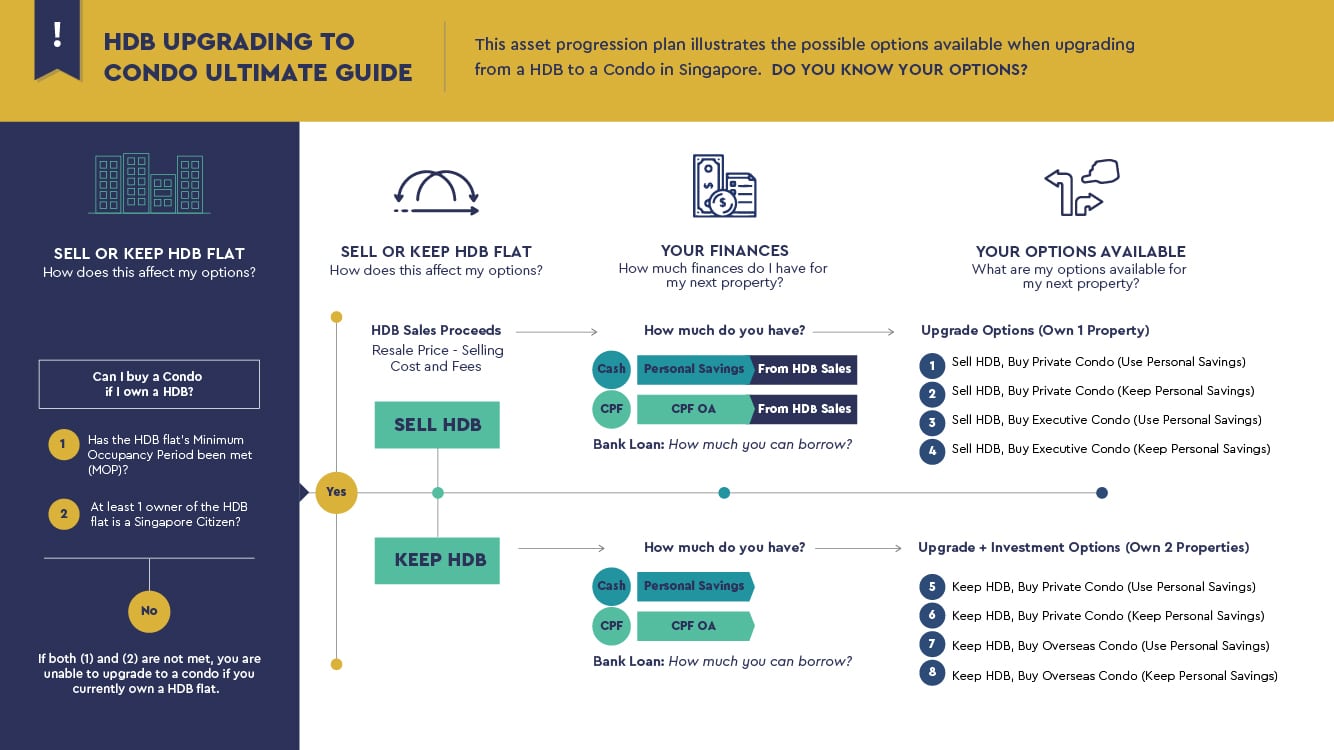

Before you begin, you ought to consider your eligibility in purchasing or upgrading to a condominium. You will only be able to buy a condominium if you have met the following requirements: reaching the Minimum Occupation Period (MOP) of living in your HDB for five years, and that at least one of the registered homeowners is a Singapore Citizen. Once you have cleared these requirements, you may begin to contemplate if you wish to retain or sell your flat. There are four basic sources for you to fund your purchase: cash, personal savings, Central Provident Fund (CPF) from the Ordinary Account, as well as taking a bank loan. You have to consider how readily available these funds are to you before you proceed to purchase your new home. For instance, bank loans are dependent on your income, determining how much the bank is willing to lend you. Selling your flat will allow you to properly fund your purchase of a condominium, with sales proceeds as another channel to being able to pay for it. Should you choose to sell your HDB and upgrade, you may purchase either a private condominium or an executive condominium with the option of using or keeping your personal savings. On the other hand, keeping your HDB allows you to purchase either a private condominium or an overseas condominium, also with the option of using or keeping your personal savings. In totality, selling your HDB renders you with one property, while keeping it leaves you with two properties under your name. And there you have it, a basic overview of purchasing a condominium. If you have any further queries, feel free to contact us, with a no obligation, no charge consultation on the options available to you.

Before you begin, you ought to consider your eligibility in purchasing or upgrading to a condominium. You will only be able to buy a condominium if you have met the following requirements: reaching the Minimum Occupation Period (MOP) of living in your HDB for five years, and that at least one of the registered homeowners is a Singapore Citizen. Once you have cleared these requirements, you may begin to contemplate if you wish to retain or sell your flat. There are four basic sources for you to fund your purchase: cash, personal savings, Central Provident Fund (CPF) from the Ordinary Account, as well as taking a bank loan. You have to consider how readily available these funds are to you before you proceed to purchase your new home. For instance, bank loans are dependent on your income, determining how much the bank is willing to lend you. Selling your flat will allow you to properly fund your purchase of a condominium, with sales proceeds as another channel to being able to pay for it. Should you choose to sell your HDB and upgrade, you may purchase either a private condominium or an executive condominium with the option of using or keeping your personal savings. On the other hand, keeping your HDB allows you to purchase either a private condominium or an overseas condominium, also with the option of using or keeping your personal savings. In totality, selling your HDB renders you with one property, while keeping it leaves you with two properties under your name. And there you have it, a basic overview of purchasing a condominium. If you have any further queries, feel free to contact us, with a no obligation, no charge consultation on the options available to you. 3 Top Reasons why People Upgrade to a Condominium?

With the close association of one's home ownership to their wealth, it is no surprise that Singaporeans are choosing to shift away from public housing to owning their own private properties. Yet, others also choose to upgrade their homes to condominiums for convenience as well as to be able to make passive income.

Aspirations and Dreams of Private property ownership

A private property is largely deemed with opulence, being able to afford the luxury of calling a home your own. Singaporeans are by and large, very ambitious people with many dreams and aspirations. Looking to rise towards the upper echelons of society, private home ownership plays a crucial role in validating one's wealth and status. It is hence seen as a goal that most people wish to work towards.

An investment property to Rent out for Passive Income

Others may have considered upgrading to a condominium because they have the sufficient funds of purchasing a condominium, while retaining their HDB. In turn, they are able to rent out their HDB flat and receive passive income. They will use their former house as the investment, which will allow them to grow their wealth. Do note that renting out a whole HDB flat is only allowed after you have met the 5-year MOP, so this route is open to long-time owners rather than recent buyers.

Moving nearer to the School of the Parents Choice (For their Kids)

Upgrading to a condominium may also be a result of wanting to ensure convenience for the children, as they travel to school. Condominiums these days are located at spots where many schools are just around the corner. Instead of simply looking for another HDB, people are usually more inclined to look at condominiums as their new potential home. The convenience will allow parents to spend more time with their children and ensure that travelling will not be too tiresome, which may in turn result in a loss of morale. Being located nearer to the school also allows parents to provide their children with extracurricular activities to heighten their growth and enable them to excel holistically. As such, parents choose to upgrade to a condominium because they want to be nearer to their children's school.

All in all, Singaporeans are slowly looking to upgrade to condominiums when they are able to because it is a goal of theirs, alongside other reasons such as convenience and the ability to profit off of their former home.

Can I buy a Condominium if I Own a HDB Flat?

As you contemplate on whether you should upgrade to a condominium, you may wonder if you are eligible to purchase one in the first place. Before you begin thinking about your finances, there are a couple of legal requirements you have to meet in order to be able to buy a condominium.

HDB Flat Minimum Occupation Period (MOP) Status

If you currently reside in a HDB flat, you will have to meet the Minimum Occupation Period (MOP). The MOP is the number of years you need to have stayed in the HDB before you are able to buy a condominium.

According to HDB, the period will be dependent upon the purchase mode, type of flat and the date in which the flat has been applied. If you purchased your HDB flat from HDB directly, from a developer via the Design, Build and Sell Scheme, the Selective En bloc Redevelopment Scheme (SERS) with portable SERS rehousing benefits or a resale flat bought from the open market with the CPF Housing Grant, the MOP will be 5 years.

A flat bought under SERS only, the MOP will either be 7 years from the date of selection of the condominium, or 5 years from the date of occupation, whichever may be earlier. Resale flats bought from the open market without a CPF Housing Grant is dependent on when the flat was applied for, with most flats applied for from 30 August 2010 onwards carrying a 5-year MOP. Newer BTO flats launched under the Plus and Prime classifications (from the October 2024 framework) carry a longer 10-year MOP, so check which category your flat falls under.

For flats bought under the Fresh Start Housing Scheme, the MOP will be 20 years.

At least 1 Homeowner is a Singapore Citizen

Should you have already met the MOP, you will be eligible to buy a condominium. However, in order to keep the HDB, at least one of the homeowners of the HDB has to be a Singapore Citizen. Otherwise, the HDB flat has to be sold within six months of purchasing the condominium.

If you have met these requirements, congratulations! You are eligible to upgrade to a condominium.

Sell HDB First or Buy Condo First? The Upgrader's ABSD Strategy

This is the single most important financial decision in your upgrade, because it determines whether you pay Additional Buyer's Stamp Duty (ABSD) at all. ABSD is a tax charged on top of the standard Buyer's Stamp Duty when you already own residential property. Since 27 April 2023, a Singapore Citizen pays 20% ABSD on a second residential property and 30% on a third or subsequent one. Permanent Residents pay 5% on the first and 30% on the second. Foreigners pay 60% on any residential property. On a S$1.5 million condo, the 20% second-property ABSD alone is S$300,000, so the order in which you buy and sell genuinely matters.

Route 1: Sell your HDB first, then buy the condo

If you sell your HDB flat (or at least exercise the option and time the completion) so that you own no residential property when you buy the condo, the condo counts as your first property and there is no ABSD to pay. This is the cleanest and cheapest route. The trade-off is logistics: you may need interim accommodation between selling the flat and collecting the keys to your new home, especially if the condo is a new launch still under construction.

Route 2: Buy the condo first, pay ABSD, then claim the remission

If you buy the condo before selling your HDB, you must pay the second-property ABSD upfront. Married couples who buy the new home jointly, with at least one spouse a Singapore Citizen, can apply for the married-couple ABSD remission to get a full refund, provided you sell your first residential property within 6 months. For a completed condo the 6 months runs from the purchase date; for an uncompleted (new launch) unit it runs from the issue of the Temporary Occupation Permit (TOP) or Certificate of Statutory Completion. The catch is cash flow: you must front the full ABSD (S$300,000 in the example above) and only recover it after the HDB sale completes within the window. Miss the deadline and the ABSD is forfeited.

A quick word on decoupling, since upgraders often ask about it. HDB decoupling, where one co-owner transfers their share to the other so a spouse is freed up to buy a second home, has been banned since 1 April 2016 (with narrow exceptions for death, divorce, marriage, financial hardship, medical grounds or renunciation of citizenship). Decoupling a private property is still legal, but ABSD is payable on the share being transferred, and IRAS has been clamping down hard on arrangements designed purely to avoid ABSD. In a May 2024 review of so-called 99-to-1 purchases, the authorities treated 166 of 187 audited cases as tax avoidance and imposed a 50% surcharge on the ABSD owed. Treat aggressive structuring with caution and get professional advice before going down this path.

Should I Sell or Keep my HDB Flat when buying a Condo? - 3 Things to consider

Once you have decided to upgrade to a condominium, you may begin to ponder whether your old flat should be kept or sold. While everyone's circumstances differ, this section provides a few prompts on which decision you should make with regard to your HDB flat.

1. Current Financial Situation

When you have made the decision to upgrade to a condominium, the most important question you have to ask yourself is whether you have the means of purchasing the condominium without having to sell your current HDB flat. If the answer is yes, you are open to the option of keeping your HDB flat, but remember that keeping it makes the condo a second property and triggers the 20% ABSD discussed above. If you answered no, then selling your HDB flat first is usually the sensible route, both to fund the purchase and to avoid ABSD entirely. On top of that, what major purchases will you be making in the near future, perhaps funding your child's education? You should also consider your monthly income, as it determines the loan you can take from the bank, and the amount in your CPF alongside how much of it you can actually use. These factors are considered later in the guide under 'Financial Considerations for your Condominium Purchase'.

2. Remaining lease of HDB flat

It is no secret that as HDBs become older, they start to slowly depreciate and demand for them falls. As such, it is important to consider how many years are left on your flat's lease before it returns to HDB. If you own a relatively new flat that has been upgraded and the amenities around it are in good condition, you can continue to keep your flat if you choose to. However, if you have been living there for a long time, you should perhaps start to consider putting it up for sale, because the older the flat, the harder it becomes to use CPF and bank financing against it for any future buyer.

3. Location of HDB flat

If you are looking to keep your HDB flat for the sake of renting it out and earning rental income, you have to ensure that your flat is situated in a desirable area. Renters are more drawn to flats near their workplace or schools, because that is often the reason they are renting in the first place. Consider how desirable the location of your HDB flat is by listing out the facilities nearby such as transportation, shopping centres, hawker centres and recreational areas such as parks. Bear in mind that HDB rents softened in late 2025 and vacancy sat at around 6%, so do not assume the strong rental returns seen during the 2022 to 2023 surge will repeat.

These are a few factors you may consider when deciding on keeping or selling your HDB flat. Ultimately, your finances will show whether you have the means to do so. But even then, the long-term value of the HDB flat should also be taken into consideration.

Selling your HDB Flat

What is the process of selling a HDB flat in Singapore?

Once you have set your mind to selling your HDB flat, your next move would be how exactly do you expedite this process? The following article will give you a rundown of putting your HDB flat on the market.

For starters, you will have to register your intent to sell your HDB Flat. Visit the HDB Resale Portal on the HDB website to register. Because of the Ethnic Integration Policy (EIP) which ensures a balanced mix of ethnic groups living in HDBs, the website will provide you with information with regard to who will be able to purchase your flat. After registration, you will also be able to view your flat's Singapore Permanent Resident (SPR) Quota. The SPR Quota refers to a limit on non-Malaysian Permanent Residents eligible to buy your flat. The SPR Quota at the neighbourhood level is capped at 5%, and 8% at the block level. In addition to this, you should also check if your flat will be affected by any upgrading or renewal programme. If so, the buyer will be liable to pay for the upgrading cost.

Once you have registered under the HDB portal, you are able to put up your flat online on various platforms and list it for sale with the help of a real estate professional. You will have to begin considering how to make your flat appealing to buyers. From the price, images of the flat, its furnishings as well as a convincing description of the house such as a convenient location will help boost a buyer's interest.

After you and a buyer have come to an agreement on the sale price and they have declared their interest in purchasing your flat, the next course of action would be to grant them an official HDB Option to Purchase (OTP), the only viable agreement in the sale and purchase of a flat. The buyer then has to provide an Option fee in exchange for your signed OTP. Within 21 days after the exchange, the buyer will have to confirm their purchase. After confirmation, the buyer will pay you the Option Exercise Fee before signing on the OTP form. Bear in mind that the OTP and Option Exercise Fee may be negotiated between both parties, but may not exceed S$5,000 in total.

The buyer and yourself will then have to go online to the HDB portal and submit a resale application document. The application has to be submitted within 7 days of each other's submission, both the buyer and seller. The resale application has to include the details of the OTP, the buyer and your particulars, a declaration of an existing loan with HDB or any financial institution if applicable, as well as your purchase.

Through the HDB portal, you will then have to endorse the following documents: seller's sale proceeds, acknowledgement for Upgrading Programme (if applicable), spouse Consent to Resale (if applicable) and resale documents for acknowledgement. There will also be a resale administrative fee that has to be borne by both the buyer and seller.

Once HDB has given a final evaluation, they will then provide a stamp of approval with regard to the sale of the flat. There will be a Resale Completion Appointment at HDB hub, in which legal documents will be signed and the exchange of house keys will be facilitated. HDB will then issue an approval letter which claims that you have now successfully sold your HDB flat.

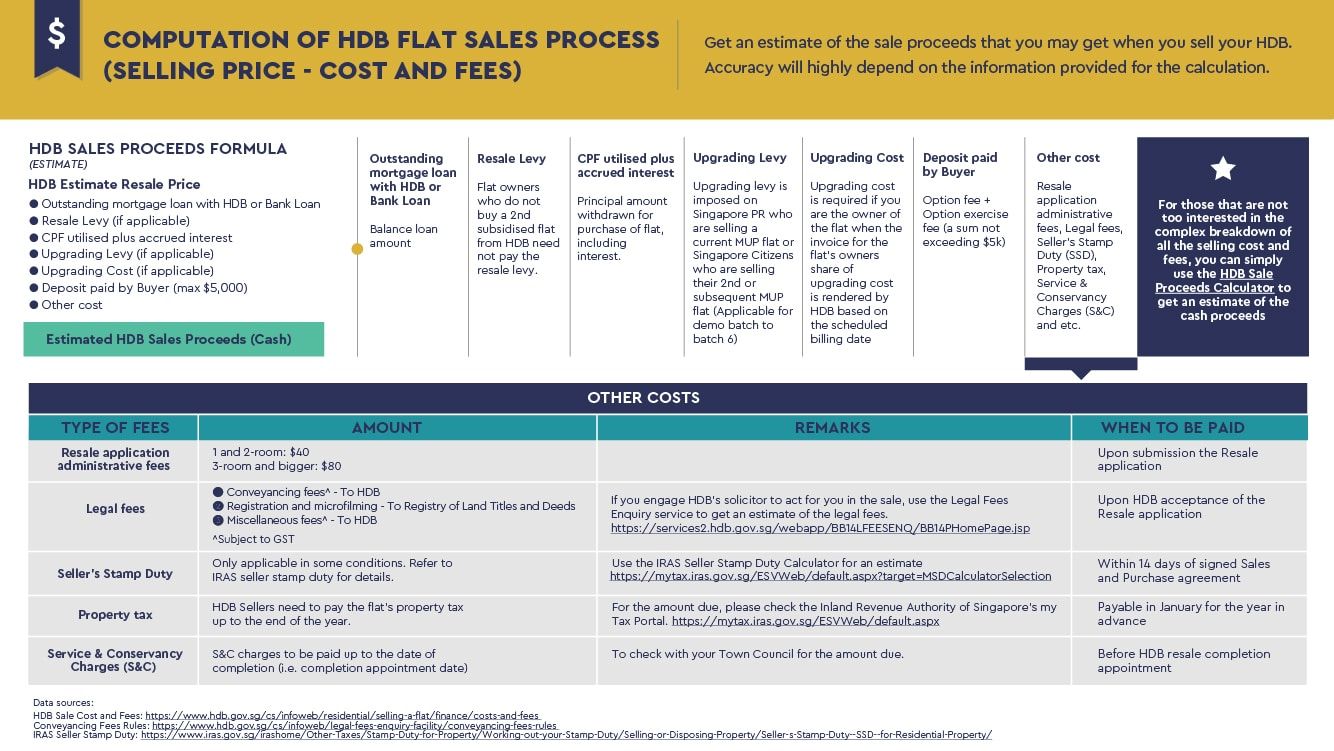

Computation of HDB Flat Sales Proceeds (Selling Price - Cost and Fees)

Financial planning is crucial when you decide to sell your HDB flat. The following article will guide you through the computation of your final sales proceeds. However, if you are not too concerned with the complex breakdown of costs and fees, you may simply utilise the HDB Sales Proceeds Calculator available on the HDB website to get an estimate of the costs.

The final sales proceeds, refers to the purchase price of your HDB flat, excluding the outstanding mortgage loan, the return of CPF funds used with accrued interest, deposit fee received previously and any other payable amounts such as resale levy or upgrading costs.

There are also a couple of outstanding payments you will have to settle as well when you sell your HDB flat.

Firstly, there is the outstanding mortgage loan, which refers to a housing loan you have taken which has yet to be repaid. To settle this, it will be deducted from the resale price of the flat should it be sufficient. Otherwise, the balance of the loan will have to be repaid in cash. Should you require information on your outstanding mortgage loan, you may visit the HDB website on financial information of purchased flats.

Secondly, if you have made a purchase of the flat with the aid of CPF monies, either as a down payment or monthly installments, it has to be returned with accrued interest into your CPF account when you have sold your flat. This cost will also be deducted from the resale price of the flat, and should it be insufficient will be covered by the fees collected (i.e: deposit fees). You may view the amount to be refunded through the CPF website under Public or Private Housing Withdrawal Details.

For those who will be purchasing a condominium or another subsidised flat after the selling of your HDB flat, you will also have to cover the fees of a resale levy. If this is your first resale of subsidised housing, the resale levy for households are as follows: S$15,000 for a 2-room flat, S$30,000 for a 3-room flat, S$40,000 for a 4-room flat, S$45,000 for a 5-room flat, S$50,000 for an executive flat, and S$55,000 for an executive condominium. As for single grant recipients, they are only required to pay half of the resale levy as stated.

There are also other costs which you may have to bear such as the upgrading costs, which will be borne if you are still the flat owner on the date the bill was issued. Should your existing flat reside in an upgraded precinct and you are a Singaporean Citizen who benefitted from the former Main Upgrading Programme (MUP) more than once, you will also have to fork out money to pay for the upgrading levy.

In addition, there are the non-refundable resale application administrative fees borne by both the buyer and seller. Legal fees are also applicable should you engage with a HDB solicitor which consists of the conveyancing fees, registration and microfilming to register land titles and deeds as well as miscellaneous fees. Without a HDB solicitor, you will only have to pay for the total discharge of the mortgage. Seller's Stamp Duty (SSD) generally does not apply to HDB sellers, because the 5-year MOP is longer than the SSD holding-period window, but the property tax owed up to completion must still be paid to the Inland Revenue Authority of Singapore (IRAS). There is also the Service and Conservancy charge which has to be paid on the date of completion.

3 Financial Considerations for your Condominium Purchase - How much can you afford? (CPF + Bank Loan + Savings)

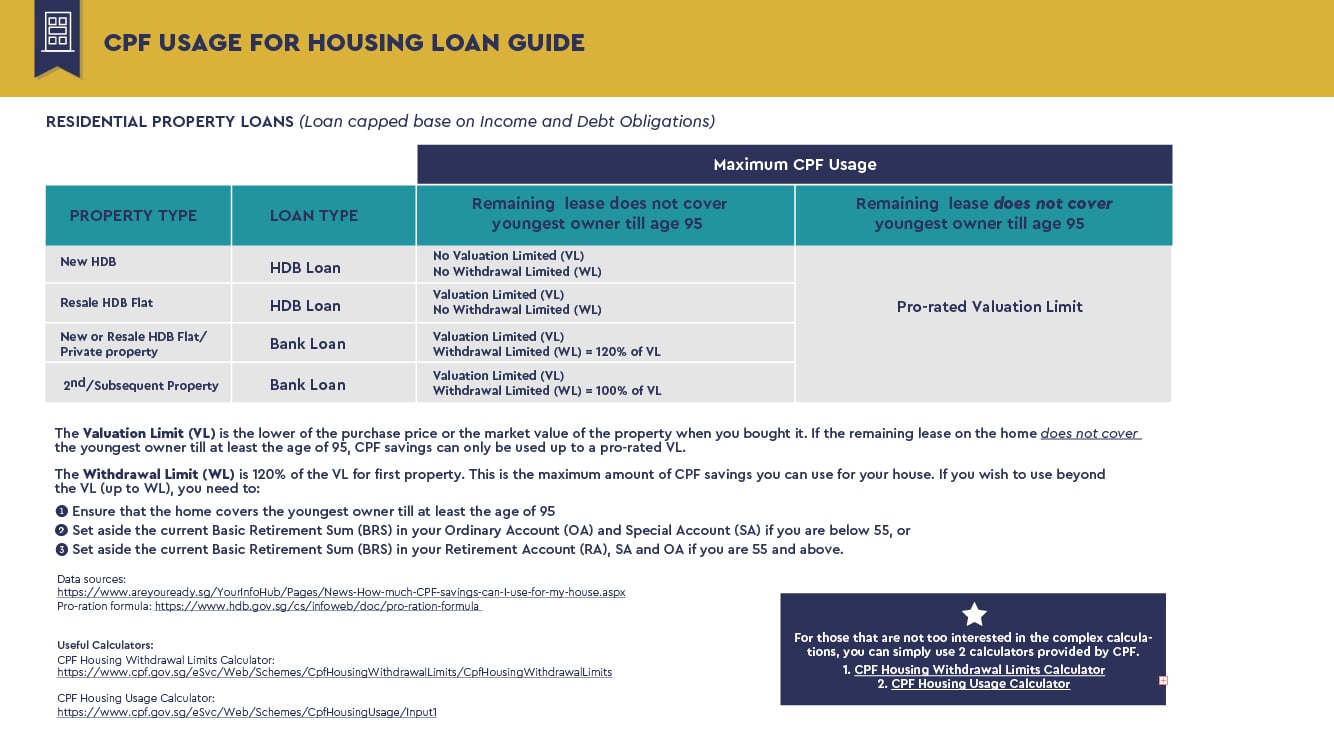

1. How much CPF can you use for your property purchase?

Purchasing a property is not a mere stroll in the park. Not only do you have to make many considerations and decisions, you need to have the financial means of being able to fund your property purchase. However, the government has put in place a savings plan named the Central Provident Fund (CPF) which can be used to fund your next property purchase.

If you are looking to upgrade to a condominium, the loan taken up will be a bank loan. The maximum CPF usage is dependent upon whether the remaining lease will be able to cover the youngest owner until they are aged 95. If it does, you are able to use up to the Valuation Limit or the Withdrawal Limit. The Valuation Limit (VL) is the lower of the purchase price or the market value of the property when you bought it. If the remaining lease on the home does not cover the youngest owner till at least the age of 95, CPF savings can only be used up to a pro-rated VL. As for the Withdrawal Limit (WL), it is essentially 120% of the VL, in other words, the maximum amount that may be used from your CPF savings.

For those who wish to use beyond the VL (up to WL), the following requirements have to be met: Firstly, the house is able to cover the youngest homeowner until they are 95 years old. Next, for those below the age of 55, you need to set aside the current Basic Retirement Sum (BRS) in your Ordinary Account (OA) and Special Account (SA). Those above the age of 55 need to meet the BRS in your OA and SA.

As for HDB flats which will take up a HDB loan, if the lease covers the youngest owner up to age 95, usage of CPF for new HDBs do not have a VL or WL. As for resale HDBs, there is a VL but no WL.

For all houses, if the remaining lease does not cover the youngest owner until they are age 95, the maximum CPF usage will be a pro-rated VL.

By and large, whether you are able to utilise your CPF in order to fund your next property purchase is dependent on a variety of factors. Depending on the property that you wish to purchase, it will affect the amount that you are able to use. HDBs will allow you to use more of your CPF as opposed to private properties. The age of the youngest owner would also greatly affect whether you are able to use a VL and WL, or a pro-rated VL. You should also keep in mind on the remaining lease of the property.

2. Bank Loan: How much bank loan can you get?

Unless you are making millions, most of us will have to take a loan from the bank when buying a condominium. Properties are not cheap, and as such we have to borrow hefty sums. Because banks have to take into account the riskiness of lending to an individual, there will be a limit to how much one can actually borrow. This section covers the factors that affect how much bank loan you may take.

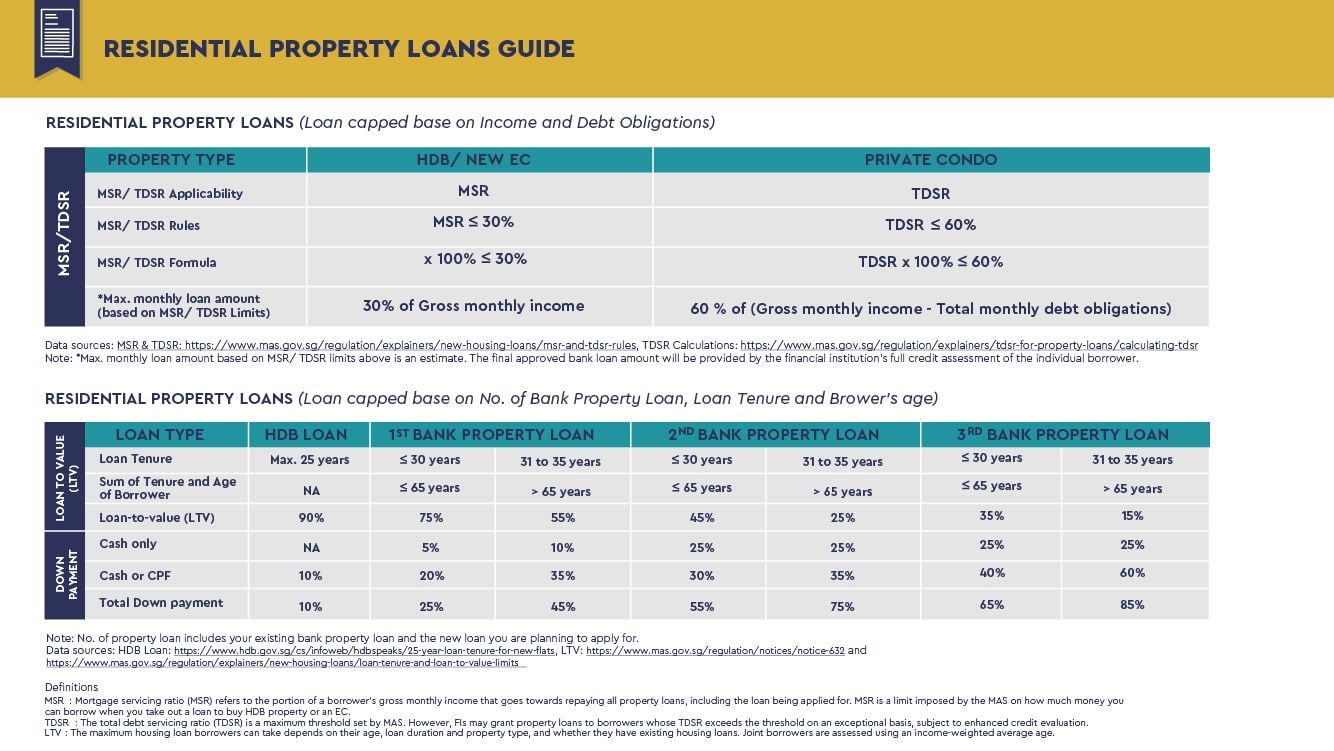

Mortgage Servicing Ratio (MSR)

MSR refers to the portion of a borrower's gross monthly income that goes towards repaying all property loans, including the loan being applied for. It is capped at 30% and applies only to HDB flats and executive condominiums bought directly from a developer (within the MOP). It does not apply to a private condominium or a resale EC bought after its MOP. To calculate the MSR, take the monthly repayment instalments for all property loans, divide by your gross monthly income, then multiply by 100%. The result must be 30% or lower.

Total Debt Servicing Ratio (TDSR)

TDSR refers to the portion of a borrower's gross monthly income that goes towards repaying all monthly debt obligations, including the loan being applied for. To calculate the TDSR, take your total monthly debt obligations, divide by your gross monthly income, then multiply by 100%. It must be 55% or lower (the cap was tightened from 60% to 55% in December 2021). Importantly, banks must stress-test your TDSR using an assumed interest rate of at least 4% for residential property, even if your actual rate is lower, so your borrowing capacity is calculated on that 4% floor rather than today's headline rates. The monthly debt obligations counted include property-related loans, car loans, student loans, renovation loans, credit card balances and any other secured or unsecured loans, including revolving loans.

Loan Tenure

The loan tenure refers to the amount of time you are given to repay a loan, dependent on the property type. The maximum loan tenure for housing loans is capped at 35 years for non-HDB properties.

Loan-to-Value (LTV)

The LTV limit determines the maximum amount you can borrow from a bank for a housing loan, as a percentage of the value of the property purchased. With no outstanding housing loan, the bank LTV limit is 75%, with a minimum cash down payment of 5% (the remaining 20% may come from cash or CPF). For one outstanding housing loan, the LTV limit drops to 45%, and with two or more it is 35%, both requiring a 25% minimum cash down payment. These limits are reduced further (to 55%, 25% and 15% respectively) if the loan tenure exceeds 30 years, or if the loan period extends beyond the borrower's age of 65. If you are instead taking an HDB concessionary loan for a flat, the HDB loan LTV limit is 75% (reduced from 80% in August 2024).

Down Payment Requirements

As an extension of the Loan-to-Value section above, your down payment can consist of cash only, or cash and CPF. For your first bank property loan at 75% LTV, you must pay at least 5% of the price in cash, with the remaining 20% payable in cash or CPF.

Cash: How much personal savings do you plan to use?

Beyond the use of your CPF and taking a bank loan, you may have to utilise your personal savings in order to fund your next property purchase.

Consider what proportion of your savings you intend to use to pay for your new house. For starters, how much does your property cost? It is important that the cost of the property is not out of your budget, as while it may be a good investment in the long run, you may encounter financial difficulties in your day-to-day finances. Next, are you currently in any financial debt? Perhaps, you may have purchased a car and you have yet to completely pay off your debts. The income you take home is also crucial in your financial planning, as it determines how quickly you will be able to pay back your loans. If you are buying the condo before selling your HDB, remember to budget for the ABSD you will have to front before claiming the remission.

Ensure that you set aside a proportion of your personal savings for situations such as in an emergency or to pay for your children's college education. It is important to remember that you should not be using most or all of your personal savings in order to pay for your new property. Keep in mind that your personal savings is there to ensure that during emergency situations, you will not struggle with your finances.

If you are unsure of how the calculations with regard to personal savings, you may wish to hire a financial consultant to advise you on how to plan your finances. They will guide you through your expenses for each month and in turn the financial considerations for the future such as the time span of being able to pay off your debts. You will be able to understand how much can be allocated to purchasing your new property, while ensuring that you do not break the bank doing so.

The Hidden Recurring Cost: Property Tax After You Upgrade

Stamp duties are one-off, but property tax is annual, and it changes depending on whether you live in a home or rent it out. This matters most if you keep your old HDB flat and lease it out while living in the condo. IRAS taxes property based on its Annual Value (AV), roughly the estimated yearly rent the property could fetch.

For the home you live in, the owner-occupier rates for 2025 and 2026 are progressive: 0% on the first S$12,000 of AV, 4% on the portion above S$12,000 to S$40,000, 6% above S$40,000 to S$50,000, 10% above S$50,000 to S$75,000, and rising in steps up to 32% for the portion above S$140,000. The government has also announced a one-off owner-occupier property tax rebate for 2026 of 15% for HDB flats and 10% for private homes, capped at S$500.

For any property you do not live in, such as a rented-out HDB flat or condo, the higher non-owner-occupier rates apply: 12% on the first S$30,000 of AV, 20% above S$30,000 to S$45,000, 28% above S$45,000 to S$60,000, and 36% on the portion above S$60,000. Factor this into your sums before assuming rental income from the old flat will be pure profit.

8 Available Options for your Next Property Purchase - Property Asset Progression Plan

As you venture into your quest to purchase your next property, keep in mind that you have a variety of options. You will have to choose either to keep your HDB flat while you purchase a new property, or sell your HDB flat and then purchase a new property. As covered earlier, this choice also decides whether you face the 20% second-property ABSD.

If you are looking to own only one property, the route would be to upgrade your home, likely a HDB flat, to a condominium. You have the choice of purchasing either a private condominium or an executive condominium. Based on your financial ability, you will decide whether to use your personal savings. If you are financially stable, you may be able to keep your personal savings while buying either a private condominium or an executive condominium. However, if you have budget constraints and cannot fully cover the costs after loans and CPF, you may have to use your personal savings.

Perhaps you are looking to hold on to the previous property and invest in a new one. In that case you may choose to purchase either a private condominium or an overseas condominium. Again, it largely depends on your financial ability to keep or use your personal savings. Remember that buying a second residential property in Singapore while keeping the HDB triggers ABSD, whereas an overseas property does not attract Singapore ABSD (though it may have its own foreign taxes).

While owning only one property is less costly, keep in mind that owning two properties enables you to earn rental income. You will be able to rent out your HDB flat, which may aid you in repaying your loans over time, bearing in mind the higher non-owner-occupier property tax noted above.

Key Condo Purchase Considerations

Executive Condo vs. Private Condo - Which is suitable for you at this moment?

You may be conflicted about whether to purchase an executive condominium or a private condominium. An Executive Condominium (EC) is a hybrid public-private property: it is not exorbitantly priced while offering comfort comparable to a private condominium. This section gives you a rundown of the factors to note as you decide.

Financial ability plays a large role in this decision. ECs are attractive because they are not as expensive as private condominiums. Eligible buyers can also receive a CPF Housing Grant on a new EC, while there are none for private condominiums, and ECs typically launch at a discount to comparable private projects, helping you save. Do note that a new EC bought from the developer is subject to the 30% MSR cap, just like an HDB flat.

However, ECs have greater restrictions than private condominiums. For one, you cannot rent out the whole EC during the MOP, and you have to fulfil the 5-year MOP before you can sell. New ECs are also only open to Singapore Citizen households at launch, then to PRs from the sixth to tenth year, and only after the tenth year (when the EC fully privatises) can foreigners buy. Moreover, private condominiums can be freehold or leasehold, while ECs come with a 99-year lease.

All in all, the condominium you choose depends largely on your financial ability and your purpose for the property. If you are financially stable and a private condominium is affordable, you may prefer that. If you have budget constraints, an EC may suit you better. It should also be noted that, with no MSR cap and no resale restrictions, a private property gives more flexibility if you wish to hold it long term or move quickly.

New Launch condo vs. Resale condo - Which should you buy?

There are so many pros and cons when it comes to purchasing a new launch condo and a resale condominium. You are able to go on for hours until the cows come home on the perks of both of these choices, but ultimately your decision should be based upon your personal preferences.

The main difference between a new launch condominium and a resale condominium would be the quality of its facilities as well as how pristine the condition of the home is. However, this may vary depending on how long it has been since the resale condominium was built. If you are someone who is not bothered by your expenses and willing to splurge on the newest and latest facilities, a new launch condominium is likely to be suited for you because it is most likely to be equipped with much fancier components. For instance, new launch condominiums are incorporating smart home technology within the homes, while resale condominiums most likely do not have this. But if you are looking for a cheaper option, a resale condominium is definitely the go-to option if you are not looking to break the bank.

In addition, new launches usually require a few years before you are able to live in it as it is still under construction. This timing matters for the ABSD remission route, since the 6-month window to sell your HDB on an uncompleted unit only starts at TOP, not at the date you signed. Resale condominiums are already built, hence you are able to make examinations of your preferences within the house as you go for a viewing, which you cannot do for a new launch.

Even then, it should also be kept in mind that new launches are likely to have smaller units as opposed to resale condominiums. This is because with the limit of land in Singapore, constructors have to work their way around this limitation which became a product of the smaller units. If you are looking to house a large family, perhaps a resale condominium will be more suited for you as you are likely to be assured that there is ample space around your home. However, if this factor is not on your radar, perhaps consider going for a new launch. The furnishings are more guaranteed to be of superb quality.

There are many factors that come into play with regard to choosing a new launch condominium. While a resale condominium has its advantages, a new launch condominium has newer facilities and features that a resale does not, and the investment horizon and remaining lease will be longer. New launches are hence deemed more attractive to buyers or potential tenants, if you are looking to sell or rent out your condominium respectively.

Condo Location - Considerations on where should you buy?

Deciding on the location of your new home should be done carefully and strategically. It is essential to keep in mind your preferences as you view the different houses, as the location of it will be a gamechanger. This article will consider the various locations across the island and which area you should narrow down to.

Travelling in this tiny island is not an issue at all. With an efficient train system, the Mass Rapid Transit (MRT) allows you to get to places rather quickly and easily. Even then, if you are travelling to the same place every day for school or for work, it may sometimes become tiring during your commute, especially if it takes more than 45 minutes to get to your destination. As such, if you travel via public transportation, you should ensure that your new home has easy access to the MRT, or a bus stop to take you to one. Moreover, you should keep in mind those more travelled places, including your family's place and the preferred school of choice for your children. This way, you are able to get to places easily. If you are someone who drives, apart from choosing a location near to places more travelled to, it is suggested that your new home should have quick access to the expressways.

In addition, it is better to have your new home conveniently located near amenities such as shopping centres, hawker centres as well as community centres, depending on your personal preference. That way, if you have to run errands or wish to take a quick bite, it is easily within reach. If you are someone who enjoys nature and or often exercise outdoors, you may wish to look for a home located near parks or trails. This way, you have easy access to take evening jogs without the hassle of travelling too far away.

As for houses you are looking to purchase as a property investment, while the aforementioned does still apply, it is largely dependent on the demographic you intend to rent the home to. However, there are a few places that are more popular than others. Houses situated near the Central Business District (CBD) area, industrial or business parks such as the Changi Business Park, Buona Vista Biopolis or the Punggol Digital District are likely to attract more buyers because it is near to where most people work. Not forgetting areas where expatriates tend to reside at include Holland Village, the East Coast and Changi area will garner more potential renters, likely because these areas are where universities are located at.

Conclusion

After reading through this guide, you should have a clearer understanding of how to upgrade from a HDB flat to a condominium. There are decisions to make, such as whether to keep or sell your HDB flat, and the order in which you buy and sell, which determines whether you pay the 20% ABSD or avoid it altogether. If you decide to sell, the guide has covered the legal processes you carry out with HDB, as well as the financial side, such as the computation of final proceeds and the costs and fees borne by buyer and seller.

There are also other ways to fund your new condominium, such as using your CPF and taking a bank loan within the 75% LTV, 55% TDSR and (where applicable) 30% MSR limits, and whether you need to dip into your personal savings. If you are unsure which type of condominium to buy, the comparison sections cover executive versus private, new launch versus resale, and which locations may suit you.

Property rules in Singapore change often, so always confirm the latest figures with HDB, IRAS and your bank before committing. If you are still unsure which options best suit your next property upgrade, feel free to contact us for a no-obligation, free assessment of the best options available to you.

Related articles

All articles →

Selling a Home Quietly: How Off-Market Deals Work in Singapore

How off-market property sales work in Singapore: why owners sell quietly, the teaser and screening process, pricing without a public launch, what…

Read more →

How GCB Ownership Actually Works in Singapore

Who can actually own a Good Class Bungalow in Singapore: the citizen-only rule, the narrow PR pathway, why companies are barred, the 65 percent trust…

Read more →

When HDB Will Buy Your Flat Back

HDB only buys flats back in three situations, and only the Lease Buyback Scheme is one you can apply for. How the scheme works, where the money goes,…

Read more →