Selling Your Condo in Singapore: A Complete 13-Step Guide (2026)

Selling your condo in Singapore? A complete 13-step guide to SSD, CPF refunds, agent fees, pricing, the OTP process and timing your next purchase right.

Key takeaways

- Sellers Stamp Duty (SSD) applies if you sell within 4 years of buying: 16% in year 1, tapering to 4% in year 4 and 0% after (properties bought before 4 July 2025 follow the older 3-year table).

- Budget for selling costs upfront: agent commission of about 2% plus GST, legal fees of roughly S$1,300 to S$3,000, mortgage redemption and any lock-in penalty.

- Your sale proceeds first repay the outstanding loan and refund the CPF you used, plus 2.5% p.a. accrued interest, so your net cash is lower than the headline price.

- Planning your next home? Sell first to buy as a single-property owner, or buy first and claim the ABSD remission by selling within 6 months (Singapore Citizen couples).

- The sale runs on the Option to Purchase: 1% option fee, a further 4% on exercise, then completion in about 8 to 12 weeks.

Selling your condo in 2026 is not quite what it used to be. Singapore's property market keeps shifting, and between cooling measures, changing legislation, and the government's close watch on prices, it can be hard to work out exactly when and how to sell.

So we put together this handbook. It is a practical, step-by-step guide to what you need to know when selling your condo today, from working out your finances to handling the legal paperwork. Get these right and you can sell with fewer surprises and walk away a happy seller.

Now that you have decided to put your property on the market, here is what to consider, in order.

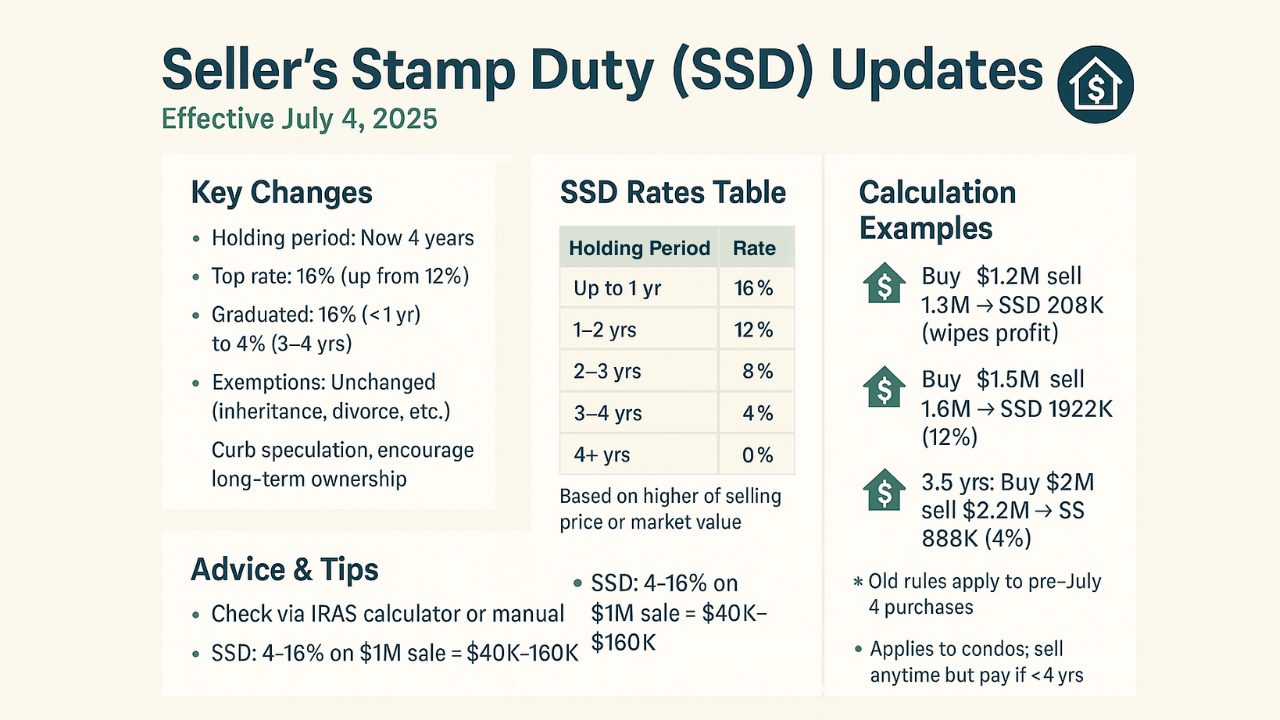

Step 1: Check the Seller's Stamp Duty (SSD) you may owe

On 4 July 2025, the government tightened the Seller's Stamp Duty rules. Here is what changed.

Key 4 July 2025 SSD changes

- The holding period was extended to four years from the date of purchase.

- The top rate rose to 16% (from 12%) for sales within a year, with graduated reductions after that.

- Exemptions stay the same for inheritance, divorce, and certain corporate restructurings (subject to IRAS approval).

These changes were made to curb short-term speculation and encourage longer-term ownership.

You are free to sell your condo at any time after buying it, but you are liable for SSD if you sell within four years. The rate ranges from 4% to 16%. On a property sold for one million dollars, that is roughly S$40,000 to S$160,000 in tax, so it is a figure you cannot ignore.

SSD is calculated on either the selling price or the market value, whichever is higher, to prevent under-declaration. One important detail: the rate is triggered by your purchase date. If you bought before 4 July 2025, the older 3-year table still applies to you. The 4-year table below applies to purchases made on or after 4 July 2025.

SSD rates for purchases on or after 4 July 2025

| Holding period from purchase date | SSD rate | Basis of calculation |

|---|---|---|

| Up to 1 year | 16% | On full selling price or market value, whichever is higher |

| More than 1 year and up to 2 years | 12% | Same as above |

| More than 2 years and up to 3 years | 8% | Same as above |

| More than 3 years and up to 4 years | 4% | Same as above |

| More than 4 years | 0% | Not applicable |

How the SSD is calculated

If IRAS assesses the market value as higher than your selling price, the higher figure is used. For example, if you sell at $1.5 million but IRAS values the unit at $1.55 million, SSD is calculated on $1.55 million.

SSD worked examples

Here is how SSD can affect your sale. For simplicity, assume the market value equals the selling price.

Sold within a year. You bought a condo for $1.2 million in August 2025 and sold it for $1.3 million in June 2026. At 16%, you owe $208,000 in SSD, which wipes out your profit.

Sold at 18 months. You bought a $1.5 million condo in September 2025 and sold it for $1.6 million in March 2027, a holding period of 18 months. That falls under the 12% band, which works out to $192,000 in tax.

Sold at 3.5 years. You bought for $2 million in July 2025 and sold at $2.2 million in January 2029, a holding period of 3.5 years. At 4%, the tax is $88,000.

Checking your SSD

You can work it out by hand, or use the IRAS Stamp Duty Calculator on the myTax Portal. Enter the purchase date and selling price, and factor the result into your timing.

Should I sell within four years?

Unless the sale promises a profit that can cover the SSD plus your other costs, such as agent and legal fees, it often makes more financial sense to hold for at least four years.

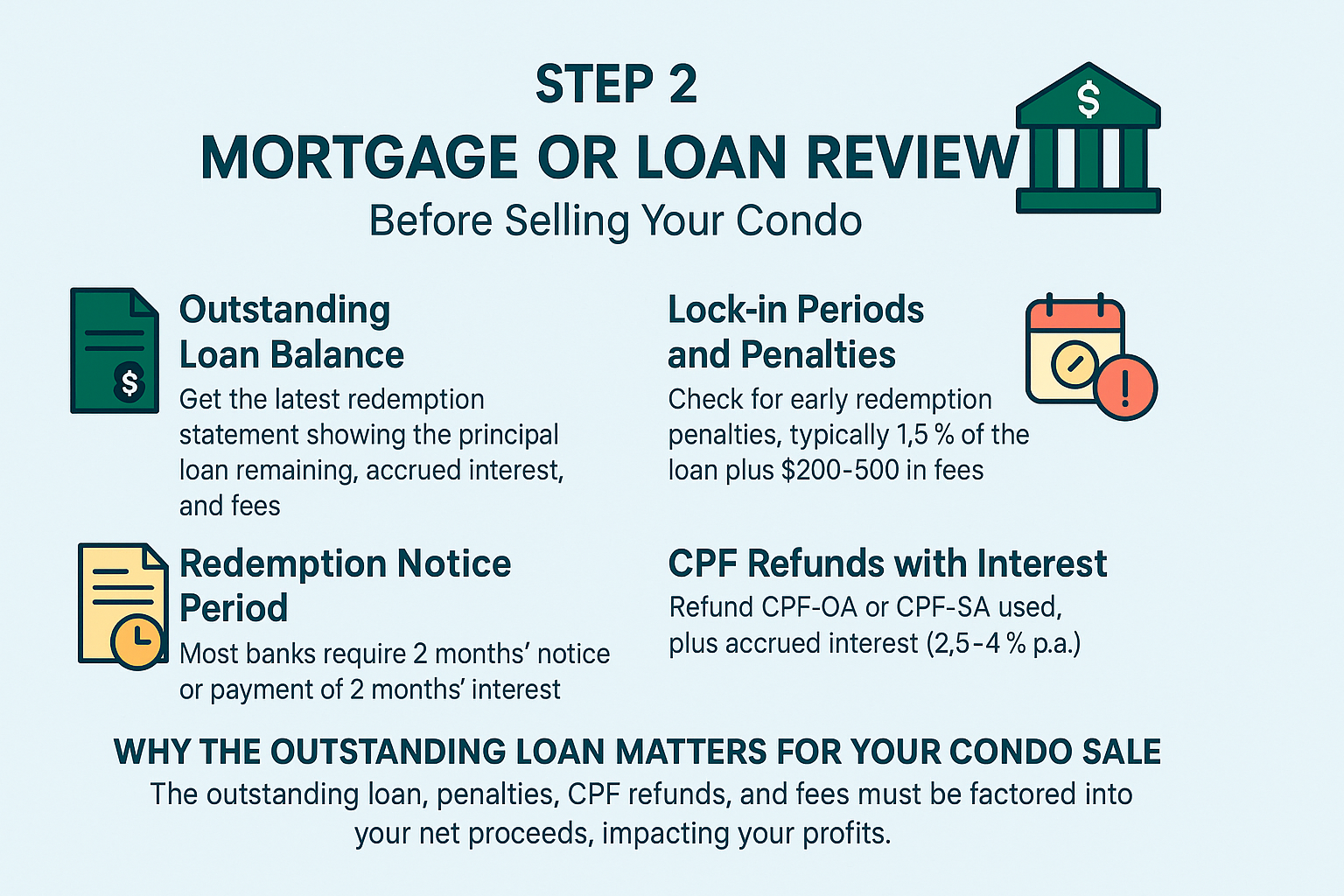

Step 2: Review your mortgage and loan before selling

Before you list, check your outstanding loan balance, understand any lock-in periods and penalties, serve the required redemption notice, and plan for CPF refunds if you used CPF for the property.

Most banks in Singapore require a structured redemption process, usually handled by your lawyer, to discharge the mortgage when the sale completes. Missing this can lead to cash shortfalls or delays.

Let us look at each factor.

Outstanding loan balance

Get the latest redemption statement, which sets out the remaining principal, accrued interest, and any fees. This matters because the proceeds from your sale must settle this first. You can request it from your bank or check your account online.

Lock-in periods and penalties

Many home loans have a two or three-year lock-in, and redeeming early to sell will trigger a penalty. The standard penalty is 1.5% of the outstanding loan plus admin fees of roughly $200 to $500. Some packages waive the penalty if you redeem after the lock-in period, but always confirm with your bank.

Redemption notice period

Banks usually require two months' written notice for redemption, or payment of two months' interest in lieu. The notice runs from the notice date to the intended redemption date, which is normally your completion date.

CPF refunds with interest

If you used your CPF Ordinary Account for the property, whether for the downpayment, instalments, or stamp duties, you must refund the amount withdrawn plus accrued interest, pegged at 2.5% per annum for the Ordinary Account.

That accrued interest is what the money would have earned in CPF had you not used it. The refund goes back to your CPF accounts. If the proceeds are not enough to cover it, no cash top-up is required, but your overall CPF balance is reduced. For sellers above 55, any excess may go to the Retirement Account.

Why the outstanding loan matters

Your outstanding loan, any penalties, CPF refunds, agent and legal fees, and any SSD all come out of the sale price when you calculate your net profit. A headline price can look high until you net off these costs. Review them before deciding whether switching packages with the same bank, or refinancing, makes sense ahead of a sale.

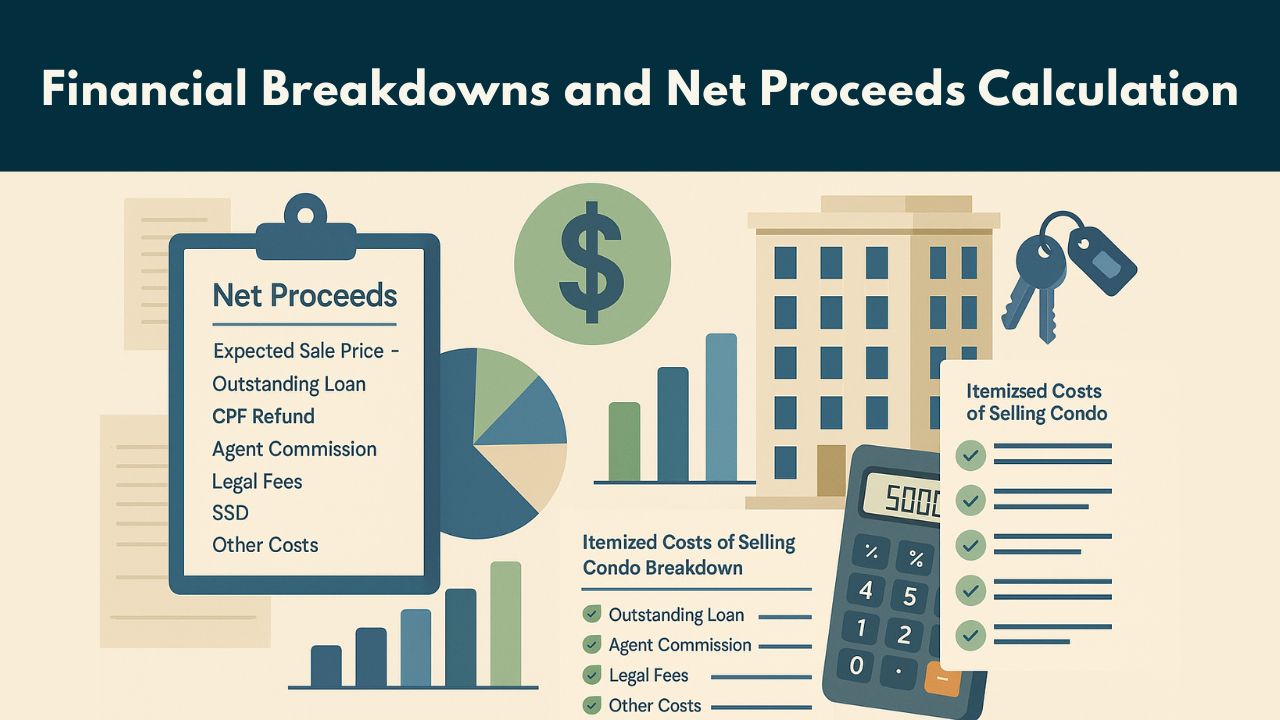

Step 3: Work out your costs and net proceeds

Depending on why you are selling, you will need to factor in other costs and plan the timing. If you are moving, for instance, account for any rental cost between selling your current home and moving into the next one.

You also need to line up the timing of your sale proceeds, any CPF refunds, and the payment dates for your new property if both transactions run back-to-back.

A common mistake is forgetting that the proceeds must first repay the outstanding home loan. Overlook this and you can end up short of cash for the downpayment on your next place.

Calculating net proceeds

Working out your net proceeds is essential for planning your finances. A simple way to frame it:

Net proceeds = expected sale price minus (outstanding loan + CPF refund + agent commission + legal fees + SSD + other costs).

This accounts for all the cash that flows out. You can firm up the numbers using the calculators from IRAS, CPF, and your bank. Be precise, as a small miscalculation can leave you short.

Itemised cost breakdown

To illustrate, here is a table of typical costs for selling a $1.5 million condo, excluding GST where noted.

| Cost category | Description | Estimated amount | Notes |

|---|---|---|---|

| Outstanding loan | Principal plus accrued interest to the redemption date. | Varies with the loan (for example, $800k remaining) | Add early redemption penalties if within lock-in (1.5% of the loan plus $200 to $500 admin fees). |

| CPF refund | Principal withdrawn plus accrued interest (2.5% per annum, Ordinary Account). | For example, $200k principal plus interest accrued over the holding period | Refund to your CPF accounts is mandatory; no cash top-up if proceeds cover it. |

| Agent commission | Fee for marketing and closing the sale. | About 2% of the sale price ($30k on $1.5M) plus 9% GST | Negotiable; about 2% is common for condos. Paid at completion. |

| Legal and conveyancing fees | Lawyer handles the discharge, contracts, and CPF. | $1,300 to $3,000 | Typical range for private property; includes stamp duty processing. |

| Seller's Stamp Duty (SSD) | Tax if sold within 4 years (purchases on or after 4 July 2025). | Up to 16% of the price (for example, $192k on a $1.5M sale held 18 months) | See the SSD section above. Payable within 14 days of exercising the OTP. |

| Other costs | Property tax proration, MCST fees, valuation, moving and minor repairs. | $1,000 to $5,000 | Valuation runs about $500. Prorate taxes and fees to the completion date. |

As you can see, these costs add up. Use the IRAS and CPF calculators to be sure you have accounted for everything before you commit to a price or a timeline.

Step 4: Research the market to set your price

Next, decide on your asking price. Do some online research and pull recent transacted prices for similar condos in your area. That gives you a realistic range so you can price competitively from the start.

You can also engage a reputable agent who specialises in private property. Experienced agents use Comparative Market Analysis (CMA) to gauge your unit's market value.

Understanding Comparative Market Analysis (CMA)

A CMA is a structured evaluation that compares your condo with similar units nearby that are sold, listed, or still on the market. A solid CMA helps you set a competitive price that attracts buyers without leaving money on the table.

Unlike simple online research, a CMA adjusts for the differences between units, so you avoid overpricing (which makes a unit hard to sell) or underpricing (which costs you). Agents can also draw on official URA transaction data and combine it with on-site observations for better accuracy.

Key factors in a CMA

Beyond location and size, here are the main variables a CMA weighs.

| Factor | Description | Effect on pricing |

|---|---|---|

| Unit size and layout | Built-up area, number of bedrooms and bathrooms, and how efficient the floor plan is. | Larger, efficient units command more; a well-laid-out unit beats a cramped one of similar size. |

| Floor level | High versus low or mid floor; penthouses and ground units are distinct. | Higher floors tend to fetch more for the view and privacy; low floors may be discounted for noise. |

| Facing and orientation | North-south versus east-west, and whether views are blocked. | Preferred facings and unblocked views sell for more; west-facing units can be discounted for heat. |

| Renovation and condition | Quality of the kitchen, flooring, and finishes, plus general upkeep. | Well-maintained, recently renovated units sell for more; dated, worn units less. |

| Age and lease tenure | Age of the development and remaining lease. | Newer freehold or 999-year units generally fetch more than aging leaseholds. |

| Proximity to amenities | Distance to MRT, schools, malls, and parks, plus condo facilities. | Prime, well-connected locations command a premium. |

| Market trends | Sales velocity, inventory, days on market, and the interest rate climate. | A buyer's market softens prices; check the latest URA reports. |

Why you should not rely on portals alone

Portals like PropertyGuru, 99.co, and EdgeProp are useful, but they mostly show asking prices, which can sit well above actual transacted prices. They can also carry outdated or unverified listings and miss off-market deals. For accuracy, use URA's free transaction portal or the SRX X-Value tool.

Lean too heavily on portals and you may form unrealistic expectations. Price too high and your unit can sit unsold.

The value of an on-site assessment

On top of the CMA, have your agent inspect the unit in person. They can spot features that data misses, such as a particular view or custom built-ins, and advise you on what buyers in your area actually want.

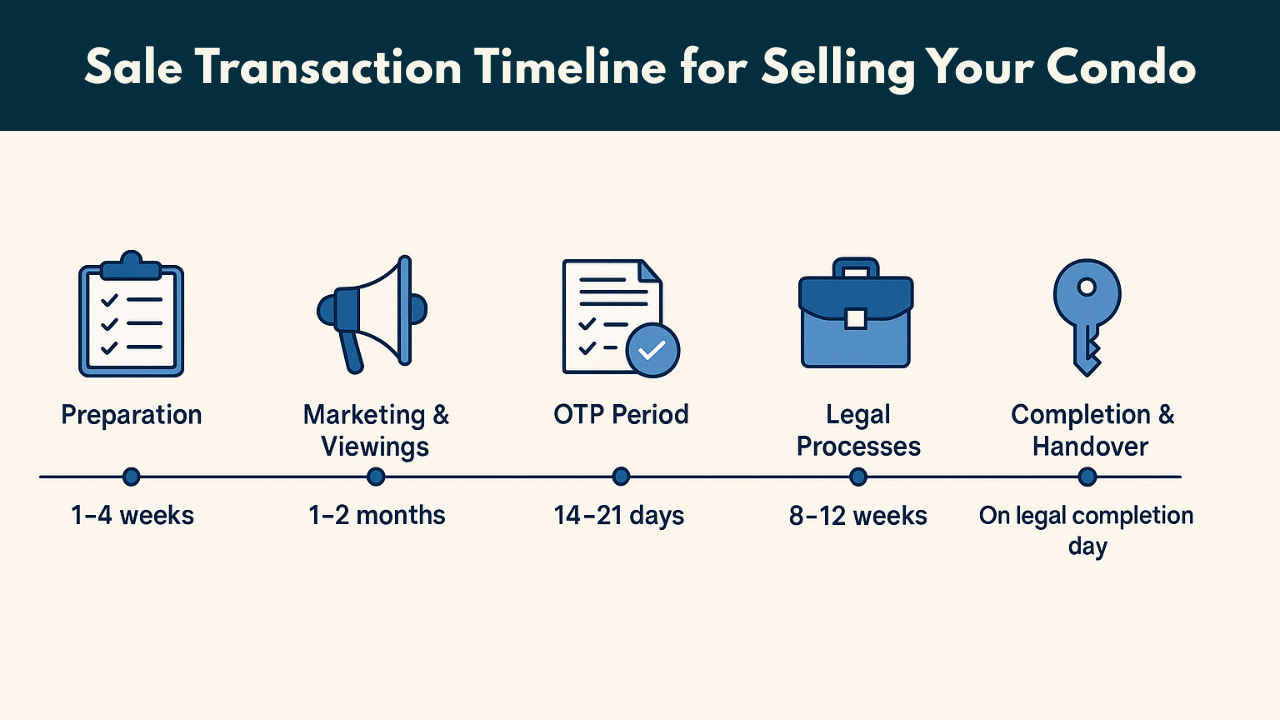

Step 5: The full transaction timeline

Depending on your price, market demand, and how prepared you are, selling a condo usually takes about three to four months from listing to completion. Here is a rough timeline.

| Phase | Duration | Key milestones |

|---|---|---|

| Preparation | 1 to 4 weeks | Check SSD, review your loan and CPF position, value the unit via a CMA, choose an agent, and prepare the home for viewings. |

| Marketing and viewings | 1 to 2 months | Set the strategy (photos and video, portal listings, social ads), run viewings, and field offers. |

| OTP period | About 14 days | Issue the OTP (1% option fee); the buyer exercises with a further 4% (5% total), making the deal binding. Verify the buyer's loan approval to reduce risk. |

| Legal process | 8 to 12 weeks | The lawyers handle the Sale and Purchase Agreement, loan redemption, CPF refunds, fees, and the title transfer. |

| Completion and handover | On completion day | Funds are disbursed, ownership transfers, and you return the keys and access cards for a clean handover. |

Step 6: Choose the right agent

The right agent can make a real difference. One who specialises in private property can take care of the heavy lifting, from marketing and paperwork to viewings and tracking the timeline through to completion. A good agent lets you sell with far less effort on your part.

Just as important, a good agent helps you get a strong price, shortens time on the market, and handles negotiations. Commission is typically about 2% of the sale price, plus GST.

What to look for in an agent

Some factors to weigh:

Track record. Review past sales in your district and condo type, success rates (such as days to sell and percentage of asking price achieved), testimonials, and references.

Market knowledge. Check their condo expertise, grasp of current local trends, CMA pricing approach, and CEA registration. Specialists handle nuances like lease decay and amenities, which helps avoid mispricing.

Marketing strategy. Ask for a clear plan for listing your unit, ideally with quality photos and video and listings on the major portals. Strong marketing can cut time on the market and support a better final price.

Communication. Responsiveness builds trust. An agent who is slow to answer calls or messages does not inspire confidence.

Negotiation. A skilled negotiator both secures a good price and resolves friction. Confirm CEA compliance and check there is no undisclosed dual representation.

Red flags to watch for

Signs of an agent to avoid:

- No valid CEA registration. All agents must be registered; check the CEA Public Register. Unlicensed practice is illegal.

- Pushy or vague tactics. Pressure to sign an exclusive agreement quickly, or no clear marketing plan and no references.

- Poor reviews. Recurring complaints on Google, PropertyGuru, or forums about delays, miscommunication, or overpromising.

- Delegation without oversight. If junior staff do most of the work, make sure the lead agent stays involved.

Step 7: Prepare your condo for viewings

You only get one chance at a first impression, so make it count. You do not need a full renovation; you can present your home well with a few quick, simple touches.

Before any viewing, make sure the unit is clean, cool, and well lit. Small fixes, like a flickering bulb, a loose hinge, or a minor blemish, add up.

Simple staging tips

Small tweaks make a difference. A quick checklist:

- Declutter.

- Use neutral decor.

- Add a few plants.

- Keep the air fresh.

- Light each room to flatter it.

- Stage a spare room as a home office.

- Keep the entrance tidy.

- Use a professional photographer to capture the unit at its best.

Why presentation helps

A well-presented condo photographs better, draws more interest online, and tends to convert more of those clicks into actual viewings. That matters most for units with unique layouts or standout features, which appeal to buyers who value how a home looks and feels.

Step 8: Market your property

Once your finances are sorted and the unit is ready, list it on the popular portals, such as PropertyGuru, 99.co, SRX, and iProperty.

A few pointers.

Invest in professional visuals

Your photos have one job: to get buyers in for a viewing. Hire a photographer for shots that show space, natural light, every room, and any standout features. Add a video walkthrough or virtual tour so buyers can explore before they visit.

Use more than one channel

Beyond the portals, consider social media, open houses, and targeted paid ads based on factors like age, income, and location.

Step 9: Negotiate and secure a buyer

Good negotiation is central to a strong outcome. Balance a competitive price with sensible concessions to close quickly while protecting your bottom line.

Evaluate and respond to offers

Beyond price, gauge a buyer's readiness through their loan in-principle approval (IPA) and overall financial stability, which lowers the risk of them backing out. Turn down lowball offers politely, and counter with other levers, such as a faster completion date.

Try to understand the buyer's motivation and build rapport. You are both working towards the same goal: a completed transaction.

Handle counteroffers and multiple bids

Use genuine selling points, like a high floor or recent renovation, to justify your price without putting buyers off. Where there are multiple bids, keep the process transparent and ethical through your agent. Know your floor price from the CMA and your cost estimates so you do not make emotional decisions.

Hold firm without scaring buyers off

You can support your price by creating a sense of momentum, for instance with well-timed open houses, while staying flexible enough not to alienate buyers. Incentives such as a flexible handover date or prorated MCST fees can help bridge a gap.

Lean on your agent's experience

A seasoned agent reads buyer signals, times counters well, and draws on past deals. They can also flag risks, such as a buyer without an IPA, and tap their network to surface better offers.

Step 10: Issue the Option to Purchase (OTP) and collect the option fee

Happy with an offer? Now you or your agent can issue the Option to Purchase (OTP), setting out details like the address, the price, and the option period during which the buyer can exercise the option.

When you issue the OTP, you collect a 1% option fee to lock in the deal. Once you have collected it, you cannot issue another OTP to a different buyer.

Buyers and sellers can negotiate a longer option period or a higher option fee. The terms in the OTP can be adjusted as long as both sides agree.

Useful OTP clauses

The OTP is a legally binding document that reserves the property for the buyer during the option period, typically 14 days but extendable. Spell out any special clauses for your situation, such as an extension of stay after completion, inclusion of furnishings, or a tenancy handover.

It is good practice to verify the buyer's IPA before issuing the OTP, to reduce the risk of them backing out.

Step 11: Wait for the buyer to exercise the OTP

After the option period, the buyer exercises the OTP. At that point they pay a further 4% of the price as the exercise fee, bringing the total deposit to 5% (the 1% option fee plus the 4% exercise fee). From here, your lawyer takes over.

If the buyer does not exercise the OTP

If the buyer does not exercise within the option period, or backs out, the OTP simply lapses and you keep the 1% option fee. You are then free to relist or offer an OTP to another buyer.

After the OTP is exercised

Once exercised, the deal is binding. Your lawyer manages the Sale and Purchase Agreement and works with the buyer's lawyer to vet documents and handle the loan redemption, CPF refunds, and outstanding items like property tax or MCST dues.

Legal completion typically takes 8 to 12 weeks, ending in fund disbursement, transfer of ownership, and physical handover.

Step 12: Appoint a conveyancing lawyer

When you sell property in Singapore, you need a conveyancing lawyer to ensure the transfer to the buyer is done legally and in line with the rules. They handle the paperwork and liaise with the bank, the buyer, and the buyer's lawyer.

This comes at a cost. Agent commission is typically about 2% of the price plus GST, and conveyancing fees are roughly S$1,300 to $3,000.

What the lawyer does

Beyond the paperwork, your lawyer manages the mortgage redemption by obtaining statements from your bank, coordinates the CPF refund including accrued interest, and handles the transfer of the title with the Singapore Land Authority (SLA).

They also prorate outstanding payments such as MCST fees, property tax, and any parking charges.

Choosing a conveyancing lawyer

Pick a lawyer with a proven track record in condo sales. Look for solid experience with mortgages and tenancies, a habit of meeting deadlines with the authorities, clear communication, and a transparent fee structure.

The lawyer and the OTP

Though not always done, you can appoint your lawyer early to review the OTP before it is issued. That is especially useful if the OTP carries special clauses, such as an extension of stay, inclusion of furnishings, or a tenancy handover.

Once the OTP is exercised, your lawyer runs the 8 to 12-week process to completion. That covers preparing and coordinating the Sale and Purchase Agreement, ensuring proper fund disbursement, handling the loan redemption and CPF refunds, and overseeing the handover.

Step 13: Complete the sale with a final inspection

From the day the OTP is exercised to completion day, keep the property in the same condition. You can invite the buyer to do a final inspection before completion, or after you have moved out.

Finally, hand your keys to your lawyer to pass on to the new owner.

Congratulations, your condo is officially sold.

After legal completion

There are a few loose ends to tidy up after completion.

Post-sale admin

Update your residential address with ICA via Singpass, and notify your banks, insurers, telcos, and any memberships and subscriptions. SingPost's Mail Redirection Service helps catch anything you miss.

Frequently asked questions

How long does the selling process take?

Usually three to four months: 1 to 4 weeks for preparation and marketing, a couple of weeks for the OTP, and 8 to 12 weeks for legal completion. A slow market or an unready buyer can add time.

When do I receive my sale proceeds?

On completion day for the cash portion. Any CPF refund (principal plus 2.5% per annum accrued interest) goes back to your Ordinary Account, typically within about two weeks.

What fees are payable?

Legal and conveyancing fees of roughly $1,300 to $3,000, agent commission of about 2% of the price plus GST, bank redemption costs ($200 to $500 admin plus a 1.5% penalty if you are still in the lock-in), and prorated MCST and property tax.

Is SSD applicable?

Yes, if you bought on or after 4 July 2025 and sell within four years: 16% within the first year, 12% in the second, 8% in the third, and 4% in the fourth. If you bought before 4 July 2025, the older 3-year table applies.

What is the minimum holding period?

Four years to avoid SSD on purchases made on or after 4 July 2025. Also check your mortgage lock-in (usually two to three years), as redeeming early can cost about 1.5% of the outstanding loan.

How do I avoid ABSD on my next purchase?

If you sell your current home first, you buy your next property as a single-property owner. If you buy first, married Singapore Citizen couples buying jointly can apply for ABSD remission, which refunds the ABSD if you sell your first residential property within six months. Speak to your lawyer about your specific situation.

Ready to Sell Your Condo? Let's Chat

If you are weighing up whether to sell, or you just want to talk it through, we are happy to help. No pressure and no hard sell, just a friendly chat to understand your situation and point you in the right direction.

Chat with us on WhatsAppRelated articles

All articles →

Downgrade From Condo to HDB in Singapore (2026): The Rules After the Wait-Out Removal

The 15-month wait-out period is gone. The updated 2026 guide to downgrading from a condo to an HDB flat: the new rules, the 30-month wait that…

Read more →

130A Lorong 1 Toa Payoh Crest HDB for Sale | Near 3 MRT Lines

Explore Toa Payoh Crest at 130A Lorong 1 Toa Payoh, a modern HDB near 3 MRT lines, top schools, and MacRitchie Reservoir. Ideal family home in a…

Read more →

Boosting Property Value Through Strategic Maintenance: A Singapore Owner's Guide

How smart maintenance, renovations, and detailed records protect and grow your Singapore property value, cut vacancies, and keep units…

Read more →