What Happens to Your Home Loan When You Sell Your Property in Singapore (2026)

Selling a Singapore home with a loan outstanding? How mortgage redemption, CPF refunds, SSD, lock-in penalties and bridging loans work at completion in 2026.

Key takeaways

- When you sell, the sale proceeds first repay your outstanding home loan so the bank can discharge its charge and the buyer gets clear title.

- If you funded the purchase with CPF, you must refund the principal you withdrew plus the accrued interest (2.5% per annum) back into your CPF Ordinary Account at completion.

- Selling early can trigger Seller's Stamp Duty. For homes bought on or after 4 July 2025 the holding window is four years: 16% within the first year, then 12%, 8% and 4%, and 0% after four years.

- Redeeming inside a loan's lock-in period usually means a penalty of about 1.5% to 3% of the outstanding amount, plus possible clawback of legal-fee rebates.

- Rates have eased into 2026 (fixed home loans around 1.8% to 2.2%, SORA near 1%), which changes the maths on refinancing versus redeeming.

Selling your property in Singapore isn’t as simple as finding a buyer and handing over the keys. You’ll also have to consider one important aspect that many miss, and that is the outstanding home loan. Whether you are paying off a mortgage, a bank loan, or an HDB loan, the outstanding amount needs to be sorted out before the sale is complete. Failure to do so can lead to withheld proceeds or IRAS penalties!

In this blog post, we’ll share all you need to know about redeeming mortgages, using bridging loans for simultaneous buy-sell transactions, and managing the legal fees associated with the sale.

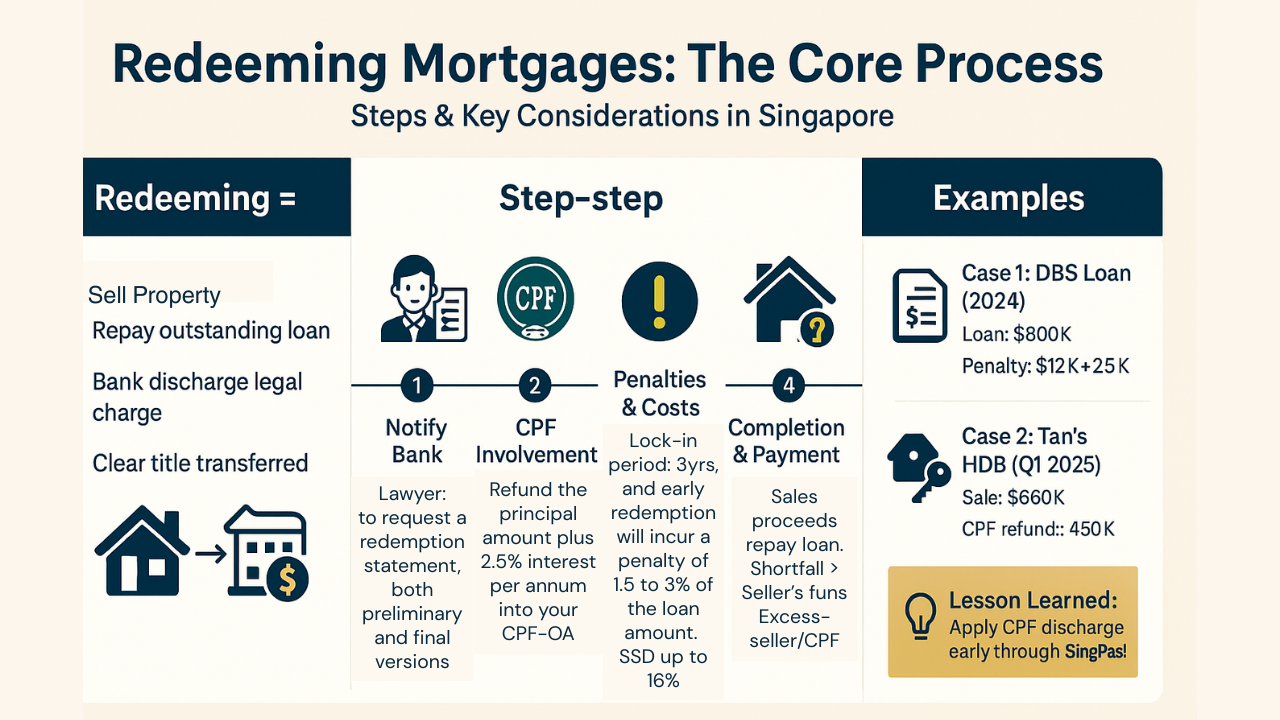

Redeeming Mortgages: The Core Process

Redeeming your mortgage means selling your property, then repaying the outstanding home loan balance, and transferring a clear title to the buyer. In Singapore, this is mandatory at completion, which is about 8 to 12 weeks after the Option-to-Purchase (OTP). The bank will then discharge its legal charge on the property with the Singapore Land Authority (SLA) or HDB.

Here’s a step-by-step guide on how to redeem your mortgage.

Notify Bank: Tell your lawyer to request a redemption statement, both preliminary and final versions. This will show the outstanding principal, accrued interest as of the completion date, and any penalties.

CPF Involvement: If you’ve used your CPF, you must refund the principal you withdrew plus the accrued interest of 2.5% per annum back into your CPF Ordinary Account (OA). Apply through the CPF Board, and it should be processed within five working days. For HDB flats, HDB will have to approve the redemption, and for private properties, the bank will approve it.

Penalties and Costs: Some loans have a lock-in period of one to three years, and early redemption will incur a penalty of 1.5 to 3% of the loan amount. For example, that’ll be S$15,000 on a million-dollar loan. Clawback of subsidies like legal fee rebates will apply. There is no capital gains tax to deal with, but Seller's Stamp Duty (SSD) applies if you sell within the holding period, which is set by when you bought.

Seller's Stamp Duty (SSD): For residential properties bought on or after 4 July 2025, the SSD holding period is four years: 16% if you sell within the first year, 12% in the second year, 8% in the third year, 4% in the fourth year, and 0% after four years. Homes bought between 11 March 2017 and 3 July 2025 follow the older three-year table (12%, 8%, 4%, then 0%). HDB flats are effectively unaffected because the five-year Minimum Occupation Period is longer than the SSD window.

Timeline and Payment: On completion day, the sales proceeds will settle the loan. Any shortfalls require your personal funds, and excess funds go to you or your CPF.

Here’s a worked example.

A seller redeems an $800,000 DBS mortgage, facing $12,000 in penalties for an early exit during the lock-in plus $2,500 in legal fees. A sale price of $1.2m covers it, and $397,500 is refunded to CPF (the principal withdrawn plus accrued interest).

Here’s another example.

Tan sold his OCR HDB flat that he purchased in 2018 for $650,000. The outstanding loan, funded by CPF, is $400,000. Redemption required refunding the $400,000 plus $50,000 accrued interest to CPF. However, an incomplete CPF application held back completion by 2 weeks and cost $1,000 in buyer penalties.

The lesson?

Apply for your CPF refund and discharge early through Singpass!

Bridging Loans: Bridging the Gap Between Sale and Purchase

Bridging loans are meant to help your financial flow during a simultaneous buy-sell transaction. They provide short-term financing of a maximum of six months, as mandated by the Monetary Authority of Singapore (MAS). This will help you cover your down payment or shortfall. They are interest-only and secured against your existing property, and you must pair it with a new home loan.

Bridging-loan rates are typically pegged to each bank's prevailing rate and sit above standard home-loan rates. With SORA near 1% and fixed home loans around 1.8% to 2.2% in early 2026, bridging rates have come down from their earlier highs but still carry a premium, so check the live quote with each bank. You can get a loan for up to 25% of the new property price or the sales proceeds from the old property, whichever is lower.

Types:

Capitalised Interest: Interest accrues and is added to the principal, and you’ll repay the whole sum after the sale. This is ideal for cashflow relief, as you don’t have any monthly payments until you sell your old property.

Simultaneous Repayment: You’ll pay the interest monthly along with your existing mortgage. With this way, you’ll pay a lower total interest, but have a higher financial burden.

Eligibility: To be eligible for a bridging loan, you have to be a Singaporean citizen, PR, or a foreigner with local property above 21 years old. You’ll need good credit and the Option-to-Purchase for the new property.

Documents: You have to prepare a few documents to apply for the loan. You’ll need the exercised OTP, CPF statements, loan balance, and caveat on the old property.

Costs: There are no processing or prepayment fees, but legal and valuation fees range between $500 and $2,000, while late fees incur a 3 to 5% + 2% penalty.

Repayment: Use your sales proceeds to repay the loan, or you might risk foreclosure on your property. CPF cannot directly repay bridging loans, but refunds after the sale can offset the amount.

Here’s a case study to illustrate a bridging loan.

A couple upgrading from HDB to an RCR condo (S$1.2M) needed a S$240,000 down payment. They took a S$200,000 capitalised bridging loan from UOB. Their HDB flat was sold in 4 months for S$700,000.

They then used the proceeds to repay the loan plus $6,000 interest. The risk is that if the HDB flat wasn’t sold within the six-month loan period, they would face 5% late fees, which amounts to $10,000. Thankfully, their flat sold early and they could repay the loan in time.

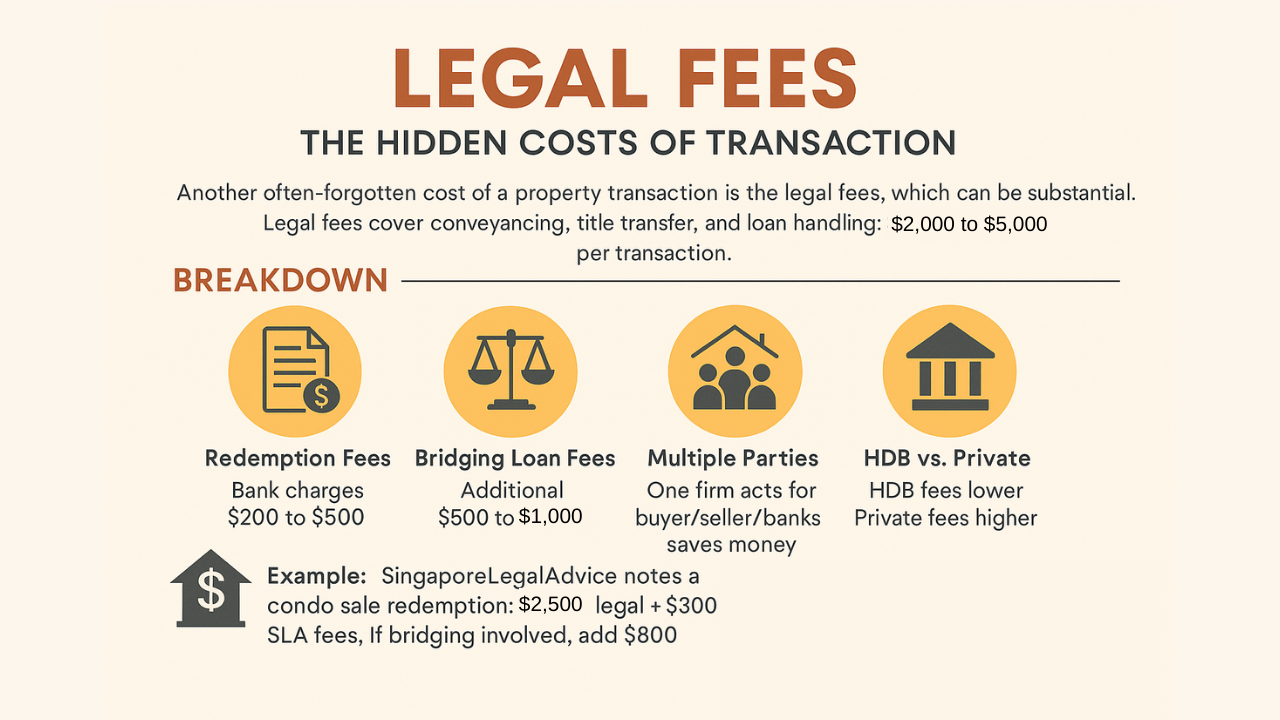

Legal Fees: The Hidden Costs of Transaction

Another often-forgotten cost of a property transaction is the legal fees, which can be substantial. Legal fees cover conveyancing, title transfer, and loan handling. These fees are typically $2,000 to $5,000 per transaction. For sales, the fees are $1,500 to $3,000 base rate plus any additional disbursements, like $500 for searches or stamps. You can use your CPF funds for legal fees if they are property-related.

Breakdown:

Redemption Fees: Bank charges $200 to $500 for discharge documents.

Bridging Loan Fees: Additional $500 to $1,000 for setup and conveyancing.

Multiple Parties: If refinancing/selling, one firm can act for buyer/seller/banks to minimize costs (e.g., $3,000 total vs. $6,000 separate).

HDB vs. Private: HDB fees lower ($1,000-$2,000), private/landed higher due to SLA lodgments.

Example: a condo sale redemption runs about $2,500 legal plus $300 SLA fees. If bridging is involved, add $800.

Here’s another case study.

Ms. Lim sold her inherited CCR condo for two million while buying a new one, using a $400,000 bridging loan. The legal fees incurred for conveyancing, sale, purchase, and loan were $4,500. The old $1.2 million mortgage had a two-year lock-in period, so Ms. Lim had to pay a redemption penalty on the outstanding balance for exiting during the lock-in.

The interest on the bridging loan added to the total cost. This was deducted from the sales proceeds, and she saved $1,000 by using one lawyer for all the transactions. A delay in the probate for an inherited property added a further $2,000 in holding costs.

Risks, Strategies, and Market Ties

Risks: A market slowdown could delay your sale, extending any bridging period and increasing the late fees incurred. Note that the rate backdrop has eased into 2026 rather than risen, with fixed home loans around 1.8% to 2.2% and SORA near 1%, so refinancing the existing loan may sometimes beat redeeming and re-borrowing. Run both numbers before you commit.

Strategies: Get pre-approval, list the old property early, and use tools like SRX for valuations. Quick, well-timed redemptions keep an upgrade on track and limit holding costs while you wait for the sale to complete.

Consult professionals: Engage CEA-licensed agents and lawyers early. Check CPF, IRAS, and banks for shifting policies, which will ensure smooth transitions in Singapore’s highly-regulated market.

Related articles

All articles →

Every Way to Sell a Property in Singapore: A Comparison

Five ways to sell a property in Singapore compared: the agented open market, selling it yourself, the auction room, the quiet off-market route, and…

Read more →

Selling a Home Quietly: How Off-Market Deals Work in Singapore

How off-market property sales work in Singapore: why owners sell quietly, the teaser and screening process, pricing without a public launch, what…

Read more →

How GCB Ownership Actually Works in Singapore

Who can actually own a Good Class Bungalow in Singapore: the citizen-only rule, the narrow PR pathway, why companies are barred, the 65 percent trust…

Read more →