Decoupling a Property in Singapore, Explained

If you've been researching property in Singapore, you've probably come across the term "decoupling." It's a strategy that allows one owner to transfer their share of a jointly owned property to the other owner, often so the outgoing owner can buy another property without being counted as an existing homeowner.

However, while it can be an effective way to avoid paying additional taxes or increase investment options, decoupling isn't suitable for everyone. It comes with legal procedures, costs, and eligibility rules that are important to understand before deciding if it's the right move.

The ABSD, or Additional Buyer's Stamp Duty, is currently at 20%, meaning that a $1.5 million condo will cost you an additional $300,000.

Hence, decoupling exists. One spouse can buy the other's share of the current home, so that the other spouse can become a first-time buyer again and avoid paying the ABSD.

What actually happens in a decoupling

The couple starts by owning one home together. One spouse then buys out the other's share, in a transfer that the law treats as an ordinary part-sale between co-owners.

After completion, the home belongs to one name alone. The freed spouse holds no residential property, buys the next one at the first-timer rate of zero ABSD, and the family ends up holding two homes while paying the surcharge on neither.

The couple has not dodged a tax. They have paid several smaller ones instead, and the whole question is whether the small ones stay small.

The four costs, priced

Buyer's stamp duty on the transferred share. The buying spouse pays BSD on the share's market value, at 1 percent on the first $180,000, 2 percent on the next $180,000, 3 percent on the next $640,000, and 4 to 6 percent above that.

Half of a $2 million condo is a $1 million transfer. The BSD works out to $24,600.

Seller's stamp duty, if the property is young. A home bought on or after 4 July 2025 carries a four-year holding period, taxed at 16, 12, 8, and 4 percent by year of exit, and the older three-year schedule of 12, 8, and 4 percent covers earlier purchases.

The transferring spouse pays SSD on the share sold if the transfer lands inside the window. On a young property, this cost alone usually kills the plan until the window closes, since 12 percent of a half share dwarfs every other line item.

Legal work, twice. The transfer needs conveyancing on both sides, plus a valuation, and where a mortgage exists the loan gets rebuilt around one income.

Budget several thousand dollars here, as the couples we see typically incur between $5,500 and $7,000 for the pair of files.

The CPF refund. Whatever CPF the departing spouse put into the home returns to their CPF account with accrued interest on completion.

The money is not lost. It is locked back into CPF, and the remaining owner must finance the home without it.

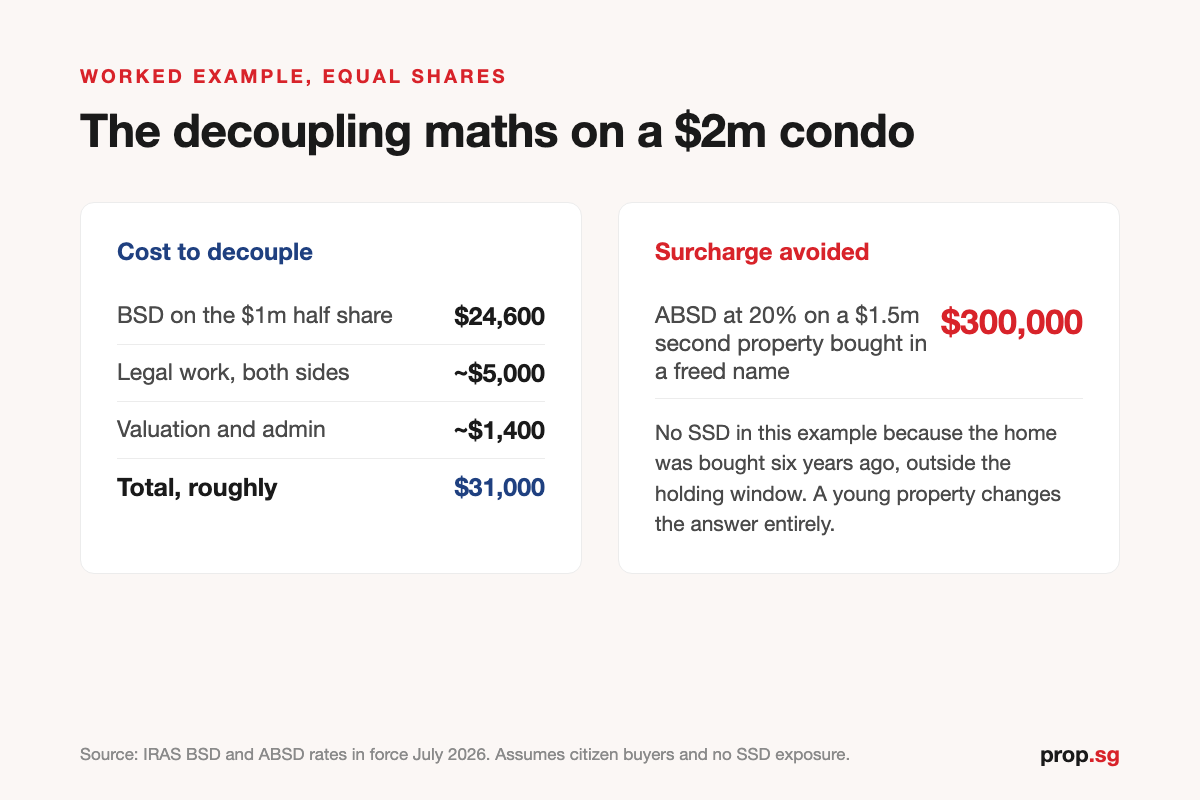

A worked example on a $2 million condo

Take a couple holding a $2 million condo in equal shares, bought six years ago, mortgage manageable on one income. The wife buys the husband's half.

| Cost | Amount |

|---|---|

| BSD on the $1 million half share | $24,600 |

| Conveyancing, both sides | $5,500 to $7,000 |

| Valuation and admin | Under $1,000 |

| SSD | None, outside the holding window |

| Total | About $31,000 |

The husband then buys a $1.5 million second property with zero ABSD. Against the $300,000 surcharge the couple never pays, the $31,000 restructuring bill is roughly a tenth of the tax avoided.

When we walk couples through this arithmetic, the concept never needs selling. The work is in checking whether any of the four costs turns hostile, and two of them can.

The two deal-breakers

A young property. Inside the SSD window, the transfer itself gets taxed like an early sale.

A couple who bought in 2025 and decouples in 2026 hands back 16 percent of the transferred share.

On the $1 million half share above, that is $160,000, and the plan stops making sense on the spot.

One income that cannot hold the loan. After the transfer, the bank underwrites the remaining owner alone, under the usual Total Debt Servicing Ratio arithmetic.

When we sit with couples on this step, it decides more cases than the taxes do. Plenty of decoupling plans die in the refinancing assessment, quietly and early, because one salary cannot carry a mortgage that two salaries chose.

HDB flats mostly cannot do this

Since 2016, most married couples have not been allowed to decouple an HDB flat, except in a few special situations. So for the vast majority of HDB owners, this isn't an option.

Instead, the planning usually happens when buying the next property. Deciding whose name goes on the new condo, and when to make the purchase, becomes the key part of the strategy.

The order of operations

In the decoupling process, the sequence of events matters. First, the transfer is completed, and the CPF refund is settled.

Then, the refinancing happens, and only then does the freed spouse sign for the second property.

Sign too early, and the count is wrong. A spouse who commits to the new purchase before the decoupling is completed can still be counted as an existing owner, and the $300,000 surcharge is applicable anyway.

The transfer will typically take eight to twelve weeks. The second purchase then proceeds on its own timeline, with the freed name clean.

The 99-to-1 question

When we review first purchases with a later decoupling in mind, the share split is the choice that gets set on day one. Couples planning ahead sometimes buy 99-to-1 rather than 50-50, so the later transfer moves a 1 percent share, and the BSD on it shrinks to almost nothing.

The way you structure the ownership split can have a real impact on your CPF usage, financing options, and what happens to the property later on. It's worth planning this carefully with a conveyancer from the start, rather than relying on tips from online forums.

Some arrangements that look like shortcuts may be viewed by IRAS as attempts to avoid taxes instead of genuine ownership setups.

What else do couples ask about decoupling?

Is decoupling legal?

Yes. It is an ordinary part-share sale between co-owners, taxed as one, and the costs above are the price of doing it properly.

Can we decouple our HDB flat?

For married couples, generally no, and the restriction has stood since 2016. Planning happens at the next purchase instead.

How much does decoupling cost overall?

For a fully held private property outside the SSD window, the usual range is in the low tens of thousands, driven mostly by BSD on the transferred share. Inside the SSD window, the picture changes entirely.

Who should be the one to exit the title?

Usually, the spouse whose income the next mortgage will lean on, and whose CPF position suits the next purchase. The remaining owner must also clear the refinancing test alone, so the decision runs on both incomes, not one.

Should we just buy the second property in one name from the start?

Where each income can carry its own mortgage, yes, buying the first home in one name and the second in the other skips the decoupling costs altogether. The constraint is that most couples need both incomes to qualify for the first loan, which is exactly how joint ownership happens.

How long does the whole process take?

Eight to twelve weeks for the transfer, refinancing, and CPF refund to settle. The second purchase follows on its own schedule.

Thinking through a second property? The stamp duty rules reward getting the sequence right the first time, so speak to the Prop.sg team before anything gets signed.

Related articles

All articles →

How GCB Ownership Actually Works in Singapore

Who can actually own a Good Class Bungalow in Singapore: the citizen-only rule, the narrow PR pathway, why companies are barred, the 65 percent trust…

Read more →

When HDB Will Buy Your Flat Back

HDB only buys flats back in three situations, and only the Lease Buyback Scheme is one you can apply for. How the scheme works, where the money goes,…

Read more →

Downgrade From Condo to HDB in Singapore (2026): The Rules After the Wait-Out Removal

The 15-month wait-out period is gone. The updated 2026 guide to downgrading from a condo to an HDB flat: the new rules, the 30-month wait that…

Read more →