Downgrade From Condo to HDB in Singapore (2026): The Rules After the Wait-Out Removal

The 15-month wait-out period is gone. The updated 2026 guide to downgrading from a condo to an HDB flat: the new rules, the 30-month wait that remains, loan limits, and the financial planning that decides the move.

Key takeaways

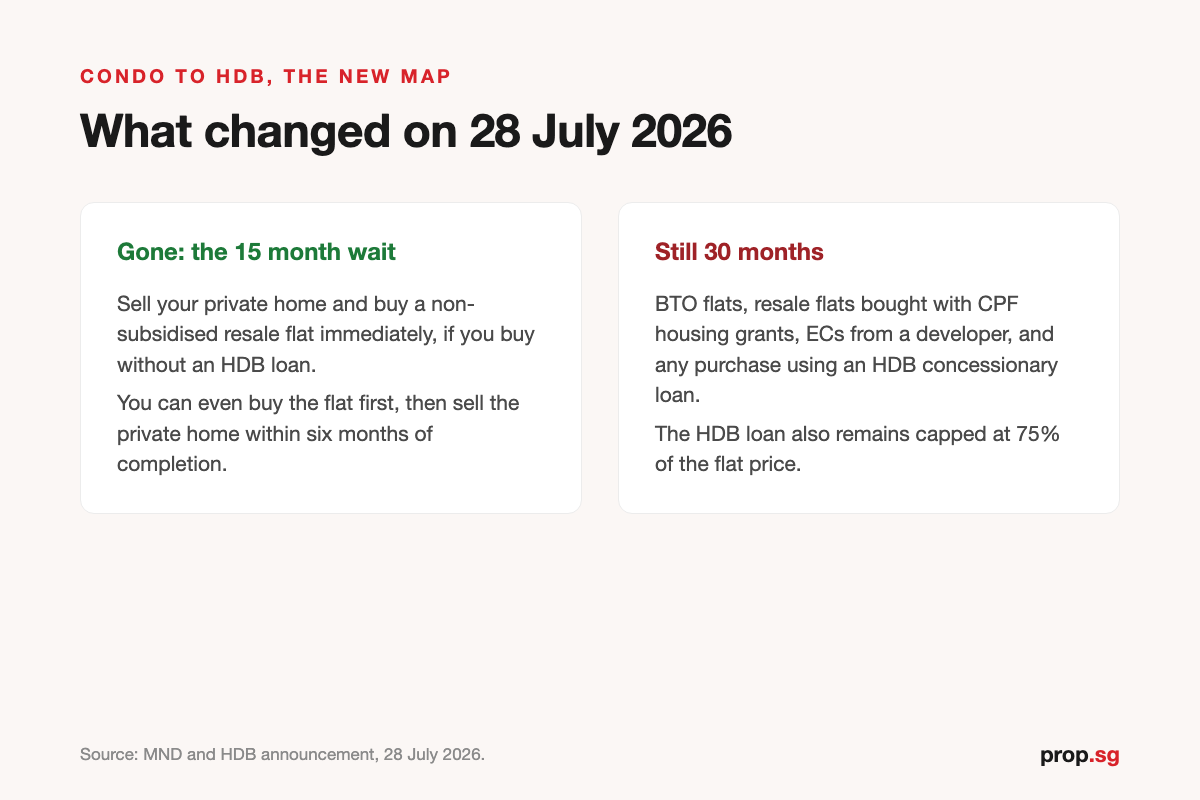

- The 15-month wait-out period has been removed from 28 July 2026, so private property owners and former owners can now buy a non-subsidised HDB resale flat immediately, as long as they do not take an HDB loan.

- The 30-month wait still applies if you want to buy a BTO flat, get CPF housing grants for a resale flat, buy an EC from a developer, or take an HDB housing loan after selling your private property.

- If you plan to keep your private property while buying a resale flat, you must sell it within six months after completing the flat purchase. This applies to properties in Singapore and overseas.

- HDB loans now cover up to 75% of the flat price, so buyers need to prepare for a larger upfront cash or CPF payment.

- Selling your condo within four years of purchase may trigger Seller's Stamp Duty, based on the rates that took effect on 4 July 2025.

- To qualify for CPF housing grants on a resale flat, your household income must not exceed S$14,000 per month.

- Your HDB loan repayment is also capped by the Mortgage Servicing Ratio (MSR), which limits monthly repayments to 30% of your gross monthly income.

If you are considering downgrading from your condo to an HDB flat, now's the time. As of late July 2026, the wait-out period is gone.

Implemented in 2022, this wait-out period used to mean that downgraders would have to wait 15 months after selling their private property before buying an HDB flat, which was a huge obstacle. Now, private property owners can easily downgrade to an HDB resale flat.

The first step in the move is usually the condo sale itself, and our step-by-step guide to selling condominium units covers that side in full. The guide below handles everything that comes after.

The biggest obstacle downgraders have faced since 2022 was removed at the end of July 2026, and the path from private property to a resale flat is now the most direct it has been in four years. Here is the updated guide, from the new eligibility rules to the financial planning, so you can decide on whether or not to make the move.

The 15-Month Wait-Out Period Is Gone

On 28 July 2026, National Development Minister Chee Hong Tat announced that the 15-month wait-out period for private property owners buying HDB resale flats would be removed with immediate effect. The measure had been introduced in September 2022 to cool a rising resale market, and the government has assessed that it has served its purpose.

Resale prices dipped slightly in the first two quarters of 2026 after more than a year of slowing growth. A much larger supply of flats reaches the end of the minimum occupation period this year, around 13,500 compared with 8,000 in 2025.

When we walk downgraders through the new rules, three points cover almost everything. What the removal of the wait-out period means is that:

- You can sell your private property and buy a non-subsidised resale flat immediately, with no waiting period, provided you are not taking an HDB loan.

- You can even buy the resale flat first and then sell your private property, as long as the private home, whether in Singapore or overseas, is sold within six months of the flat purchase being completed.

- Anyone who had a waiver appeal pending does not need to wait for a reply. You can apply for an HDB Flat Eligibility letter directly, and HDB is reaching out to applicants.

- The old exemption for those aged 55 and above moving to a 4-room or smaller flat is no longer needed, because nobody waits now on the resale route.

The 30-month wait-out period that remains is a separate rule. It applies when a former private owner wants a subsidised purchase or subsidised financing, which covers BTO flats with or without grants, resale flats bought with CPF housing grants, an EC bought from a developer, and any purchase made with an HDB concessionary loan.

Market watchers do not expect the change to send resale prices sharply upward. The demand it releases is expected to concentrate in larger flats, five-room and executive units in particular, where transaction volumes have fallen since 2022.

Forecasts for the full year sit in the region of half a percent to two percent growth. The bigger MOP supply arriving through 2026 and 2027 supports that moderation.

Eligibility To Own an HDB Flat After Selling Your Condo

When we check eligibility with sellers, two questions come to mind. What do you want to buy, and how will you pay for it?

| BTO flat, resale with grants, EC from developer, or any purchase on an HDB loan | Non-subsidised resale flat, bank loan or no loan | |

|---|---|---|

| Wait after selling private property | 30 months | None |

| Citizenship | To buy as a family unit, a Singapore Citizen plus at least one other SC or SPR | Same |

| Monthly household income ceiling | S$7,000 for a 2-room Flexi, S$7,000 or S$14,000 for a 3-room, S$14,000 or S$21,000 for 4-room and larger. Singles at least 35 years old, S$7,000 for a 2-room Flexi | No income ceiling to buy. S$14,000 family income ceiling to qualify for a CPF housing grant |

** Refer to the HDB website for the full eligibility criteria.*

Most downgraders take the resale route, and with the wait-out removed, it is now the immediate option as well as the flexible one.

The BTO route only matters if you want a brand-new flat.

In that case, the 30-month wait applies. Plus and Prime projects also carry a 10-year minimum occupation period, plus a subsidy clawback when you eventually sell.

Tightening of HDB Loan Limits

Once you meet the eligibility requirements, the next thing to consider is whether you're comfortable putting in more cash or CPF funds for your flat purchase.

In August 2024, HDB and MND announced that the Loan-To-Value (LTV) limit for HDB loans would be reduced from 80% to 75%, bringing it in line with loans from private financial institutions.

In practical terms, buyers now need to prepare a larger upfront payment to cover the difference. For example, if you're buying a resale flat priced at S$600,000, the maximum HDB loan you can take is now S$450,000 at 75%, compared to S$480,000 previously at the 80% limit.

Remember too that taking the HDB loan route as a former private owner brings the 30-month wait back into play. Most downgraders who want to move quickly will probably be looking at bank financing instead of HDB loans.

Planning Your Finances

This is a crucial step because any misguided decision would heavily impact your finances. The wait-out removal takes away the forced pause, and that makes careful sequencing more important, as you can easily make a mistake.

6 key factors to consider when mapping out your HDB homeownership finances:

- How much cash and CPF do you have after selling the condo

- How much loan can you get to buy an HDB flat

- How much is the Buyer's Stamp Duty (BSD)

- Do you need to pay a Resale Levy

- What temporary housing might still cost you

- Can you apply for a CPF grant

1. How Much Cash and CPF Do You Have After Selling the Condo

To determine the proceeds from the sale of your condo, offset the selling price against the costs of the transaction which includes:

- Seller's Stamp Duty, if you sell the condo within 4 years of buying it

- Outstanding mortgage loan

- Conveyancing fee

- Property agent fee

- Property tax

- Maintenance fee

- Accrued interest on the CPF used for purchasing the condo

Watch the Seller's Stamp Duty timeline closely as it can have a significant impact on your finances.

Under the rates that took effect on 4 July 2025, if you bought your condo on or after that date and sell it within 4 years, SSD applies at 16% within the first year, 12% up to two years, 8% up to three, and 4% up to four, falling to zero once you have held it for more than 4 years. Condos bought before 4 July 2025 follow the earlier 3-year SSD window.

Selling too soon can wipe out a large slice of your sale proceeds. Check your purchase date carefully before you commit, and be sure you sell only after 4 years to avoid paying the SSD.

Note that the CPF you used to purchase the condo is reimbursed to your CPF Ordinary Account with 2.5% accrued interest. The net proceeds after the CPF reimbursement and transaction costs arrive in your bank account as cash.

2. How Much Loan Can You Get to Buy an HDB Flat

If you need a home loan from a bank to purchase an HDB flat, you should take into account:

- Total Debt Servicing Ratio (TDSR), the percentage of gross monthly income allocated to repaying all monthly debt obligations, is capped at 55%. On a gross monthly income of S$6,000, the maximum for servicing all debts, including car and study loans, is S$3,300.

- Mortgage Servicing Ratio (MSR), the percentage of gross monthly income allocated to housing loan repayment for an HDB flat or an EC bought from a developer, capped at 30%. On the same S$6,000 income, S$1,800 can go towards the monthly mortgage.

- Loan-to-Value (LTV) ratio, the maximum share of the property price you can borrow, capped at 75% for a first housing loan. To purchase a S$600,000 flat, the maximum loan is S$450,000, and the remaining S$150,000 must come from cash or CPF-OA.

3. How Much Is the Buyer's Stamp Duty (BSD)

Buyer's Stamp Duty is payable on the purchase of both private and HDB properties in Singapore. The current BSD rate for residential property runs up to 6%, computed like this:

| Property price or market value | BSD rate |

|---|---|

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Next S$1,500,000 | 5% |

| Remaining amount | 6% |

For a million-dollar HDB flat, the calculation would be S$1,800 on the first S$180,000, S$3,600 on the next S$180,000, and S$19,200 on the next S$640,000, for a total BSD of S$24,600.

4. Do You Need To Pay a Resale Levy

If you have purchased a subsidised flat in the past, you are liable for a resale levy when buying a second subsidised flat from HDB. A subsidised flat includes a BTO flat, a resale flat bought with a CPF housing grant, a Design Build and Sell Scheme flat, or an EC from a developer.

- For first subsidised flats sold on or after 3 March 2006, the resale levy ranges between S$7,500 and S$55,000.

- For first subsidised flats sold before 3 March 2006, the levy is 5% to 25% of the resale price of the sold flat, subject to minimums of S$15,000 for a 2-room flat, S$30,000 for a 3-room flat, S$40,000 for a 4-room flat, S$45,000 for a 5-room flat, and S$50,000 for an Executive flat.

5. What Temporary Housing Might Still Cost You

This section used to matter to every downgrader. With the wait-out removed, it now applies mainly to two groups.

Those heading for a BTO flat, grants, an EC, or an HDB loan still face the 30-month wait. And anyone who sells their condo before securing the right resale flat may still want a short rental bridge.

If you do need to rent, here is a guide to HDB flat monthly rents. Open-market rents softened through late 2025, and the end of wait-out leasing may ease them further, so always check the latest HDB rental statistics before you budget:

| HDB flat type | Monthly rent |

|---|---|

| 2-room flat | S$2,300 to S$2,480 |

| 3-room flat | S$2,400 to S$3,100 |

| 4-room flat | S$3,000 to S$4,400 |

| 5-room flat | S$3,150 to S$4,300 |

For many families, a cleaner alternative is to buy first, move once, and sell the private property within the six-month window.

6. Can You Apply for a CPF Grant

First-time HDB buyers may qualify for housing grants ranging from S$5,000 to S$80,000. Whether they are buying a BTO flat or a resale unit, these grants can help reduce the loan amount and make monthly repayments more manageable.

For resale flats, families must have a monthly household income of no more than S$14,000 to qualify for CPF housing grants. However, those who previously owned private property should also take note of the 30-month wait period before they can apply for certain grants.

| Buyer's profile | Grants for new flats | Grants for resale flats |

|---|---|---|

| Singles, two or more singles | Enhanced CPF Housing Grant (Singles) | CPF Housing Grants (Singles), Enhanced CPF Housing Grant (Singles), Proximity Housing Grant (Singles) |

| Singles buying with parents | CPF Housing Grants (Singles), Enhanced CPF Housing Grant (Singles), Proximity Housing Grant (Singles) | |

| Couples, families, multi-generation families | Enhanced CPF Housing Grant (Families), Step-Up CPF Housing Grant (Families) | CPF Housing Grants (Families), Enhanced CPF Housing Grant (Families), Step-Up CPF Housing Grant (Families), Proximity Housing Grant (Families) |

Summary

With the removal of the 15-month wait-out period, moving from a condo to a resale flat is now much simpler than it has been since 2022. The good news is that you now have more flexibility with the timing.

You can sell first and buy after, or buy first and sell your condo within six months. The key is not to rush into the sale.

When we look at downgrade plans, the way you structure the move often matters more than what the market is doing.

There are still important rules to keep in mind. The 30-month wait still applies for subsidised housing options, the SSD period can affect those selling a condo too soon, and the 75% loan limit means you'll need to plan your cash carefully.

Some homeowners focus too much on their sale proceeds and forget about the costs involved in downgrading, leaving them with less financial cushion than expected.

Planning the opposite move instead? Our guide to upgrade from HDB to a condo covers that path in the same detail.

Moving from a condo to an HDB flat is definitely easier now, but it's still a decision that needs careful planning. If you're unsure about the best order of steps, the Prop.sg team has helped numerous homeowners navigate this tricky process, so give us a call.

Related articles

All articles →

Selling a Home Quietly: How Off-Market Deals Work in Singapore

How off-market property sales work in Singapore: why owners sell quietly, the teaser and screening process, pricing without a public launch, what…

Read more →

How GCB Ownership Actually Works in Singapore

Who can actually own a Good Class Bungalow in Singapore: the citizen-only rule, the narrow PR pathway, why companies are barred, the 65 percent trust…

Read more →

When HDB Will Buy Your Flat Back

HDB only buys flats back in three situations, and only the Lease Buyback Scheme is one you can apply for. How the scheme works, where the money goes,…

Read more →