How to Buy a Resale Condo in Singapore (2026): Costs, Stamp Duty and Step-by-Step Guide

Buying a resale condo in Singapore? A clear 2026 guide to LTV and TDSR limits, BSD and ABSD rates, the OTP process, SSD on resale, and the full step-by-step.

Key takeaways

- You can borrow up to 75% of the price on your first home loan, but this drops to 55% if the loan tenure runs past 30 years or beyond age 65.

- Your total monthly debt repayments must stay within the 55% TDSR limit, stress-tested at a 4% interest rate floor.

- Buyer's Stamp Duty (BSD) runs from 1% on the first $180,000 up to 6% on any portion above $3 million. Additional Buyer's Stamp Duty (ABSD) applies on top for second and subsequent homes, PRs and foreigners.

- The resale process is locked in by the Option to Purchase (OTP): a 1% option fee to secure it, then a further 4% when you exercise it.

- If you might resell, note the Seller's Stamp Duty (SSD): selling within four years of buying triggers a charge of 16%, 12%, 8% or 4% depending on how long you held it.

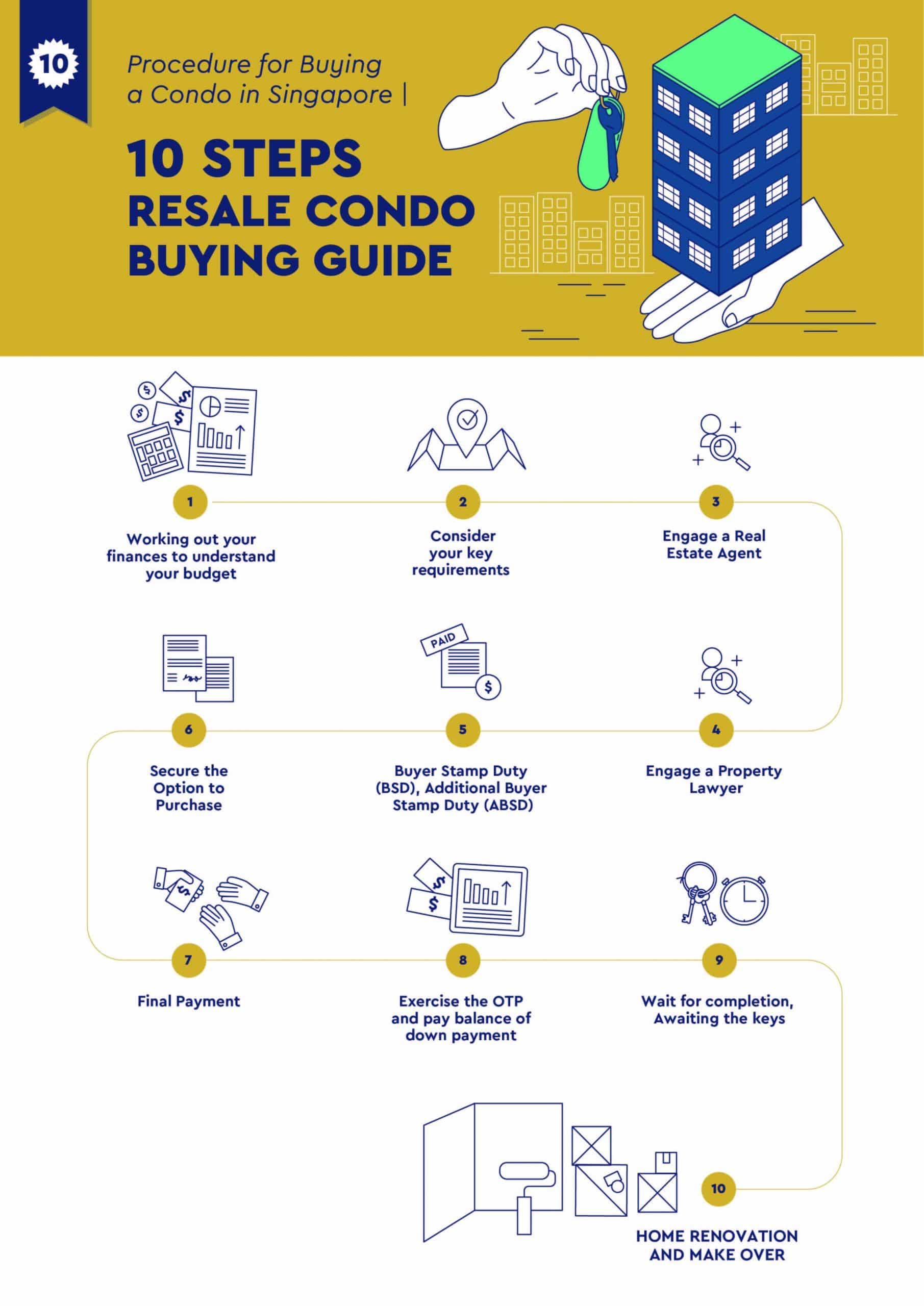

Working out your finances to understand your budget

The amount of money that you can potentially borrow depends on your creditworthiness and the Loan-To-Value (LTV) limit imposed by the Monetary Authority of Singapore. You can expect to obtain up to 75% of the property price on your first housing loan, but this is subject to the loan tenure. If your loan tenure runs beyond 30 years, or extends past the age of 65, the LTV limit on a first loan drops to 55%. Additionally, there is the Total Debt Servicing Ratio (TDSR) to consider: your total monthly debt repayments cannot exceed 55% of your gross monthly income. When the bank works out your TDSR, it stress-tests your home loan at an interest rate floor of 4%, not the actual rate you are offered, so it pays to leave some headroom.

Moreover, there is a minimum cash down payment that one has to take note of. This portion cannot be paid from your CPF account, so you have to ensure that you have sufficient cash on hand.

With reference to the financing that you are able to obtain, your real estate agent will be better able to narrow down properties that will best meet your budget.

Consider your key requirements

Attaining the home of your dreams begins with knowing what you want. All home buyers yearn for property that is able to reap generous returns. To determine the potential of a property, it is imperative for home buyers to do basic research and consider the following factors:

Freehold or Leasehold Condo

Depending on one’s risk appetite, some buyers are inclined towards freehold developments because such property tends to appreciate, and their tenure offers security to buyers. In contrast, some buyers may prefer leasehold developments for their higher capital appreciation and thus, higher yields.

Upcoming Regions and Availability of New Projects in Those Regions

Developments that are situated in areas designated for major redevelopment tend to provide better returns.

Proximity to MRT Stations

Developments that are in close proximity to MRT station(s) are able to fetch better resale values due to their potential to slash commute times for the residents.

Possible School Choices Relocation

Singapore’s distance-based priority allocation rule favors developments that are within a 2km radius from prestigious schools. To reap favorable gains from your potential property, it is thus wise to consider the location to which the good schools may possibly relocate.

Other requirements may include your budget and a convenient timeline for you to move in.

Engage a Real Estate Agent

Now that you have your requirements in mind, you will need assistance in narrowing down your options from a myriad of available ones - this is when you engage a real estate agent. A real estate agent will work with you to comprehend your requirements, subsequently creating a list of properties for your consideration. Subsequently, you may further narrow down the options on that list and start viewing the properties of your choice. Throughout the process, your agent will provide advice on aspects such as market rates and guide you along for a seamless transaction.

However, be sure to run a check on the Public Register (maintained by the Council of Estate) to ensure that you are engaging an authorized professional.

Engage a Property Lawyer

Your team of property professionals is not complete without a property lawyer. A property lawyer will assist in taking you through the complex financing and legal documentation process.

Running through contractual terms and conditions is one of the fundamental tasks of a property lawyer. Additionally, he also has to run a title search to check that the seller is the actual owner of the property. Next, he will have to send out legal requisitions to at least nine government agencies to ensure that there will not be any problems with your purchase, even in the future. After which, he will receive payment from you and exercise the Option-to-Purchase in a timely fashion.

A property lawyer also plays a crucial role in the preparation of your financing and i) making progress payments (for incomplete property) or ii) determining and making the right amount of payment needed in order to change hands (for completed property).

Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD)

The Buyer’s Stamp Duty (BSD) is a tax levied on all property buyers regardless of nationality, and it is dependent on the purchase price or market value of the property, whichever is higher (the ‘Base’). Generally, the more expensive the property, the higher the BSD rate.

For residential property, BSD is charged in tiers: 1% on the first $180,000, 2% on the next $180,000, 3% on the next $640,000, 4% on the next $500,000 (the portion above $1 million up to $1.5 million), 5% on the next $1.5 million (the portion above $1.5 million up to $3 million), and 6% on any amount above $3 million.

The Additional Buyer’s Stamp Duty (ABSD) is charged on top of BSD and depends on your residency status and how many residential properties you already own. Singapore Citizens pay 0% on their first home, 20% on a second, and 30% on a third or subsequent property. Permanent Residents pay 5% on their first home, 30% on a second, and 35% on a third or subsequent property. Foreigners pay a flat 60% on any residential purchase. These rates have applied since 27 April 2023.

To avoid or reduce your ABSD liability, your lawyer may assist you in timing the sale of your existing property with the purchase of the new property. Married couples buying a second home jointly may qualify for an ABSD refund if they sell their first residential property within six months, so speak to your lawyer about the conditions before you commit.

Secure the Option to Purchase (OTP)

After working out the BSD and any ABSD payable, you may proceed to secure an OTP. Securing an OTP involves the payment of the first option fee (1% of the purchase price of the property). The payment of this option fee prevents the seller from selling that property for a specific duration (usually two weeks).

Afterwards, when you exercise the OTP, a second payment of 4% of the purchase price is incurred (Step 8).

Final Payment

Finally, you will have to pay your real estate agent and your property lawyer.

If you are purchasing a resale unit, it is customary for the seller to pay his own agent, who will then pay your agent. If you are purchasing a new condo unit, your agent will receive his payment from the developer.

Payment to your lawyer does not only consist of his legal fees; payment will also have to be made to the Singapore Land Authority and Inland Revenue Authority of Singapore.

Exercise the OTP and pay balance of down payment

Within two weeks of securing your OTP (Step 6), you will have to exercise it. Your property lawyer will assist you with this and ensure that the OTP is exercised before the deadline.

To exercise the OTP, you pay the balance of the option fee (the further 4%). Once this payment has been made, you can then make the rest of your down payment so that your cash and CPF together cover the 25% that sits outside a 75% first housing loan.

Both option fee payments must be made in cash, while the remainder of the down payment can be paid via a combination of cash and CPF.

If you may resell later: the Seller’s Stamp Duty (SSD)

One figure worth knowing before you buy is the Seller’s Stamp Duty, because it shapes your exit plans. For homes bought on or after 4 July 2025, SSD applies if you sell within four years of your purchase date: 16% if you sell within the first year, 12% within two years, 8% within three years, and 4% within four years. Sell after holding for more than four years and no SSD is payable. If there is any chance you will move on within a few years, factor this into your sums before committing.

Wait for completion, Awaiting the keys

Once all the relevant paperwork and payments have been processed, you can officially look forward to collecting the keys to your new home. The purchase of property that is approaching its Temporary Occupation Permit (TOP) allows for a shorter wait.

Home Renovation and Make Over

Let your imagination run wild by borrowing the creative juices of interior designers. When selecting an interior designer to help you with transforming your vision into a reality, you should weigh the cost involved with the designer’s track record to reduce the likelihood of having to incur repair costs in the future.

Once the house has been designed and furnished to your heart’s desire, you may begin moving into your new home. Creating a list of all the belongings you would like to take with you and packing them in an orderly fashion will guarantee that you will have an easier time unpacking. You may engage professional movers, family or even close friends to assist you in moving bulkier items.

Summary

Purchasing a condo may seem daunting on first glance but it does not necessarily have to be if you follow the steps in this simple guide and engage a professional, reliable team.

If you’re looking to buy a condo in Singapore with professional guidance at every step of the way of your property purchase, look no further because Prop.sg is the team for you and do you know what is the best part of it all? The resale condo buyer services provided by us are completely free of charge (i.e. no commission) to you as a buyer.

Related articles

All articles →

Selling a Home Quietly: How Off-Market Deals Work in Singapore

How off-market property sales work in Singapore: why owners sell quietly, the teaser and screening process, pricing without a public launch, what…

Read more →

How GCB Ownership Actually Works in Singapore

Who can actually own a Good Class Bungalow in Singapore: the citizen-only rule, the narrow PR pathway, why companies are barred, the 65 percent trust…

Read more →

When HDB Will Buy Your Flat Back

HDB only buys flats back in three situations, and only the Lease Buyback Scheme is one you can apply for. How the scheme works, where the money goes,…

Read more →